The Era of Reaching $500M–$999M with Zero VC Meetings: Translating RBF, Crowdfunding, and AI Low-Cost Growth into Solo-Founder Scale

For those who feel VCs and bank loans are out of reach: in 2026, the funding map has been rewritten. Here's why the RBF market is ballooning to $15.86B next year, plus all three axes a solo founder can combine starting today.

What you'll learn in this article

- The key point to grasp before reading the full article

- How the issue changes practical decisions after reading

- Which follow-up article is worth opening next

Hey, listen up.

That state of “I don’t have time or connections to meet VCs, but I want capital” — it’s time to graduate from that.

Right after I went independent, I remember staring at bank loan paperwork and slumping over my desk thinking, “There’s no way this gets approved.” VCs felt like a different universe entirely — that “scene” tied to specific Tokyo neighborhoods had nothing to do with someone like me.

But when you line up the 2026 numbers, the air has completely shifted.

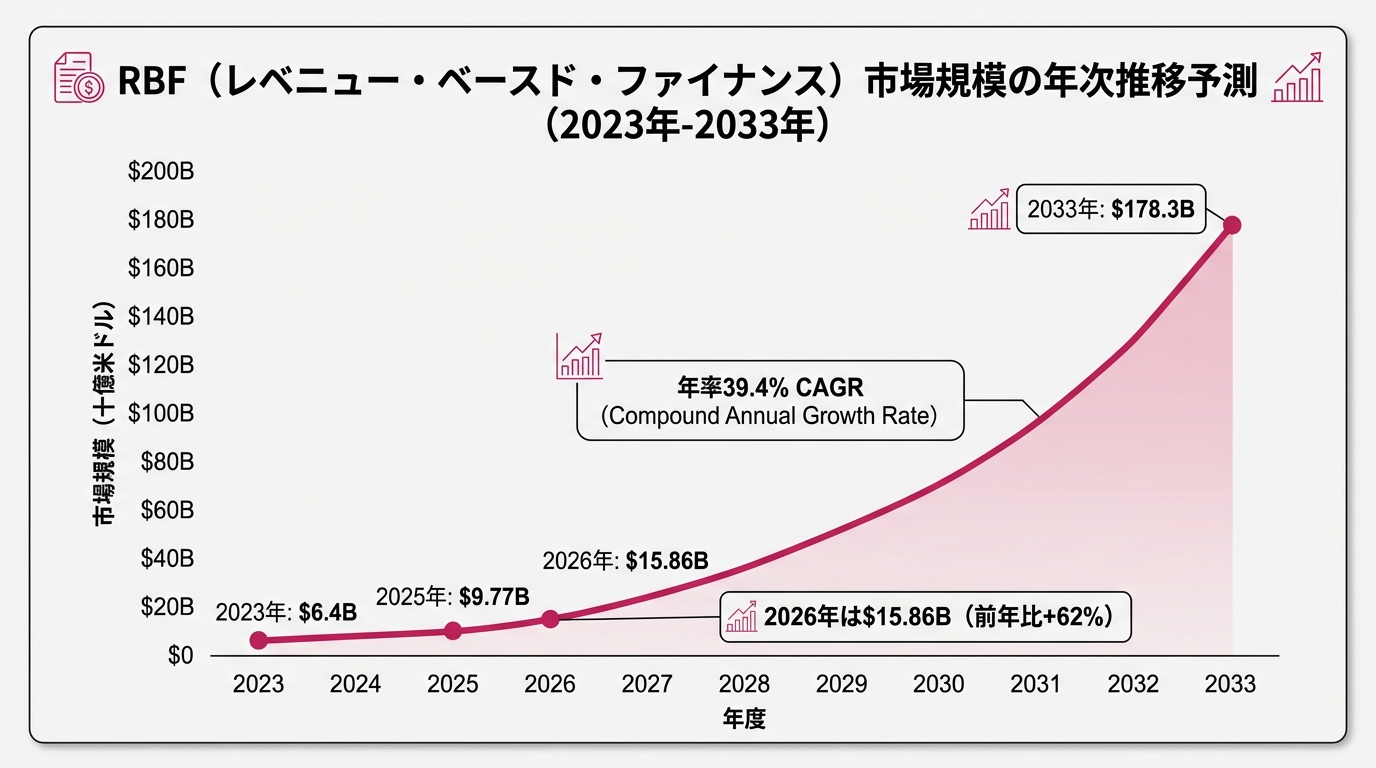

According to Allied Market Research’s 2024 report, the global Revenue Based Financing (RBF) market hit $6.4B in 2023. It’s projected to balloon to $178.3B by 2033 — a 39.4% CAGR (compound annual growth rate). Meanwhile, ResearchAndMarkets’ 2026 edition report projects growth from $9.77B in 2025 to $15.86B in 2026.

The numbers are saying one thing.

“Funding without going through a VC” is starting to become mainstream in 2026.

Yesterday, I wrote “The era of aiming for ‘$1B from day one’ is over” — about redesigning the soonicorn ($500M–$999M) as a goal that’s actually within reach. Today is the sequel. “Okay, so how do you raise the capital to get there?” — that’s the topic.

There’s a path that gets you there with zero VC meetings. I’m going to unpack all three axes, in order.

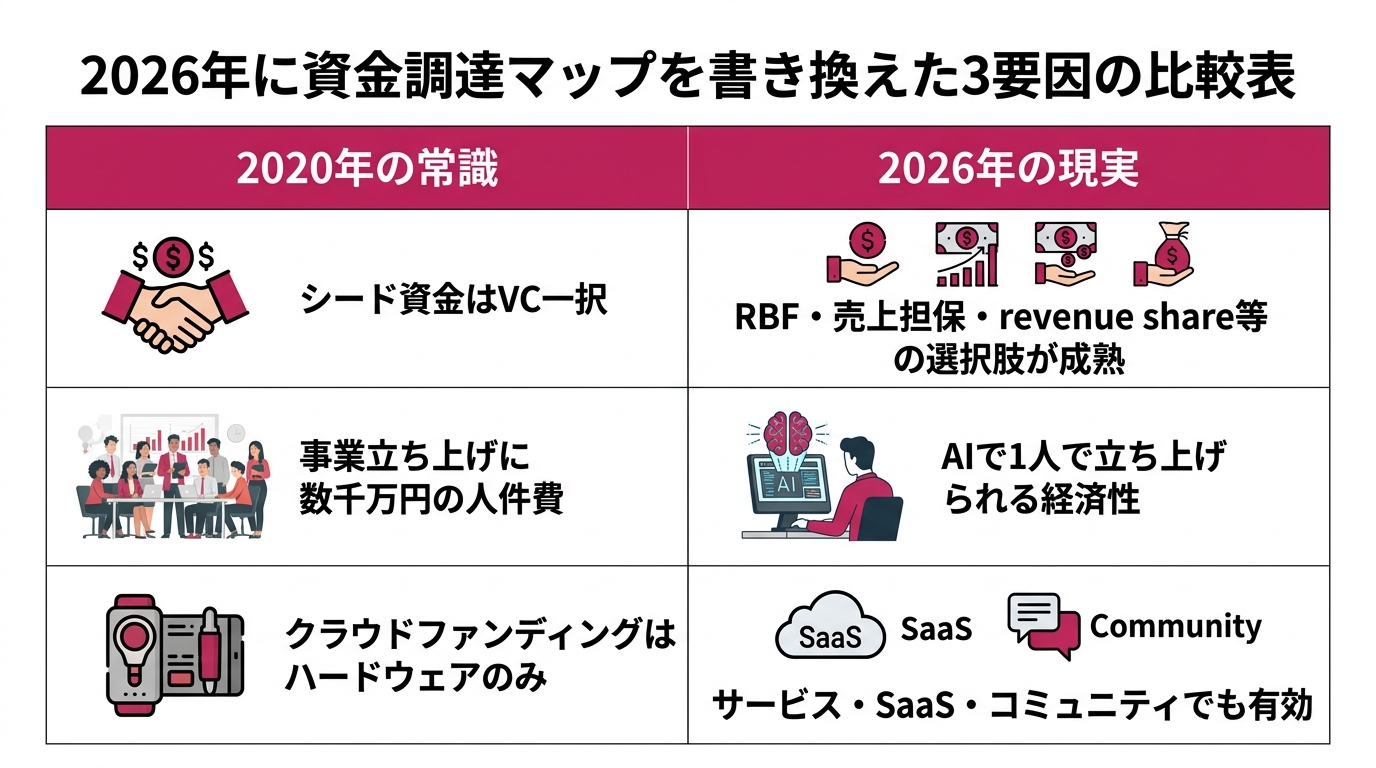

Why “no-VC” options have become realistic right now

The phrase “fundraising without relying on VCs” would have sounded like wishful thinking around 2020. Back then, the live ammunition was too small — anything seed-stage above $1M was effectively a VC-only game. That flipped in 2026.

Three reasons stack up.

First: the number of lenders offering RBF has exploded.

According to Crestmont Capital’s 2026 RBF statistics, North America alone holds 60% of the RBF market. The user base is mostly tech startups, e-commerce, and subscription businesses. Stripe Capital, Capchase, Pipe, Re-cap, Wayflyer — I’d run out of fingers listing them. The mechanism is simple: “X% of revenue goes to repayment,” with the monthly amount flexing with revenue. Zero revenue month means zero repayment.

Second: AI made the economics of “launching solo” actually work.

According to the Q1 2026 report featured by Crunchbase, $300B flowed to 6,000 startups in Q1 alone, with 80% (about $237B) concentrated in AI. But the real insight isn’t “AI startups raise easily.” The real insight is that “solo founders who use AI” have seen launch costs drop to one-tenth of what they were 2–3 years ago. Apps go live without writing code. Operations run without hiring engineers. That’s what made “launch a business without dropping VC money” feel real.

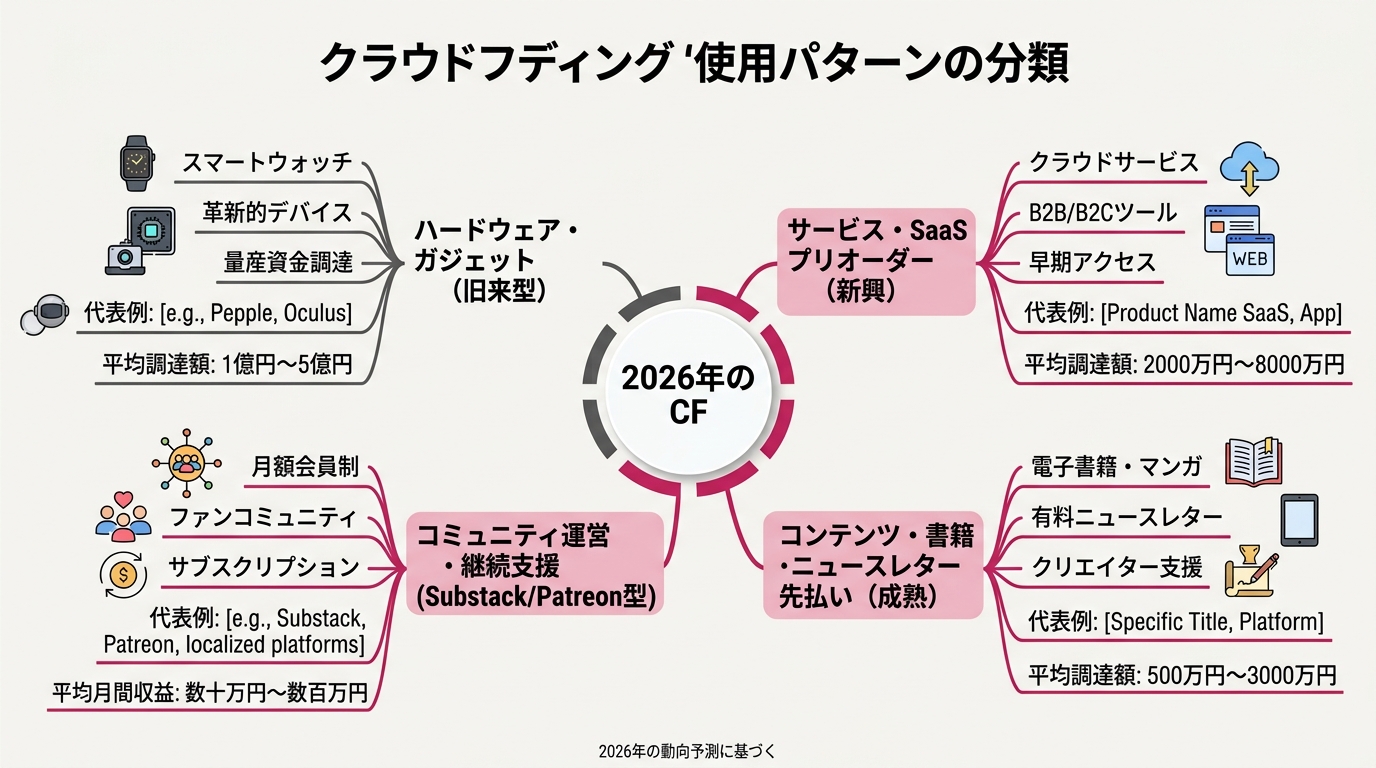

Third: crowdfunding stopped being “for hardware only.”

Looking at Kickstarter’s official annual statistics page, cumulative pledges exceeded $8B by 2025, with over 600,000 projects. The recent trend is the rise of “service, content, and community” projects. SaaS pre-orders, newsletter prepayments, community operations support — the shape has expanded.

Three tailwinds blowing simultaneously. That’s where 2026 stands right now.

Weapon 1: RBF (Revenue-Based). Don’t give up equity, repay with a slice of monthly revenue

I put RBF first because it has the best fit for solo founders.

The mechanism is simple. Decide the loan amount, then a fixed percentage of monthly revenue (usually 3–10%) goes to repayment. It ends when you hit the predetermined total repayment cap. Unlike VCs, you don’t give up equity, so you keep operational control. Unlike bank loans, it’s not a fixed monthly payment, so you don’t get cornered when revenue dips.

Three real-world examples.

First, Capchase. One of the largest RBF providers for SaaS startups. Instead of recognizing annual contract revenue monthly, Capchase pays 80–90% of the annual contract amount upfront. The startup gets cash now, and Capchase collects monthly. I know founders who said, “Instead of rushing for a Series A, I extended runway with Capchase and grew revenue first.”

Second, Stripe Capital. If you’re processing payments through Stripe, Stripe looks at your historical payment data and notifies you, “You qualify for $X.” Repayment is a percentage of payment revenue. The startup doesn’t need to assemble Excel paperwork — Stripe already sees everything, and the conversation moves from there.

Third, Pipe. A marketplace where you can sell subscription revenue as “future cash flow.” If you’re sitting on $120K in annual subscriptions, you can sell them now for around $108K. The discount is the cost, but it’s drastically cheaper than giving up equity.

RBF isn’t free money. The effective cost (IRR-equivalent) varies by platform and business size, but is generally said to be around 15–30% annually. Whether it’s “cheaper” than VC dilution depends on your business stage. My read: it fits founders in the $500K–$5M annual revenue range who want to grow cash before a Series A. Below that range, monthly repayments squeeze the business. Above it, running VCs in parallel often produces better growth — that’s my view.

If you’re thinking “I’ve never even heard of RBF,” don’t worry. It’s still not common in Japan. But if you’re a cross-border startup, you can apply to Capchase or Stripe Capital today.

Weapon 2: Crowdfunding. The mechanism where customers become “prepaying investors”

If you still think crowdfunding (CF) is “the hardware world’s thing,” your understanding froze in 2019.

The headliners are Kickstarter and Indiegogo. Beyond them, Substack (paid newsletter prepayments), Patreon (monthly community support), and Buy Me a Coffee (one-off creator support) have matured by category. The platform options for “customers paying first” have widened.

The crucial part is clarifying “what are you selling, exactly, when you use CF for fundraising?”

CF is fundraising, but its essence is “marketing plus pre-sale.” It’s a system where customers buy before the product is finished. So if a project doesn’t show “concrete value to the customer,” it won’t gather money no matter what crowdfunding platform you put it on.

Case 1: Substack pre-orders for a newsletter. Collect 10 prepayments at $120/year = $1,200, use the funds to set up your writing environment, then start writing. Don’t write first and gather readers — gather readers first, then write. This is the textbook example of “customers become prepaying investors.”

Case 2: SaaS Indiegogo pre-sale. Make just an MVP (minimum viable product) video, then pre-sell the $240/year plan at $120. Acquire the “first 100 companies” while using those funds for development. With today’s tools — Notion AI, Figma, AI coding environments — you can ship an MVP in 3 months.

Case 3: Patreon community launch. Gather 100 supporters at $10–$50/month, and you’ve got $1,000–$5,000/month in fixed cash flow. As working capital for a solo founder, that’s huge.

There’s a caveat. CF means “the moment funding lands is the busiest moment.” The obligation to deliver kicks in, so botched reward design leads to hell. I’ve watched several people get crushed by shipping logistics for half a year. The “raised the money but the founder collapsed first” pattern. So upfront physical operations design is life-or-death.

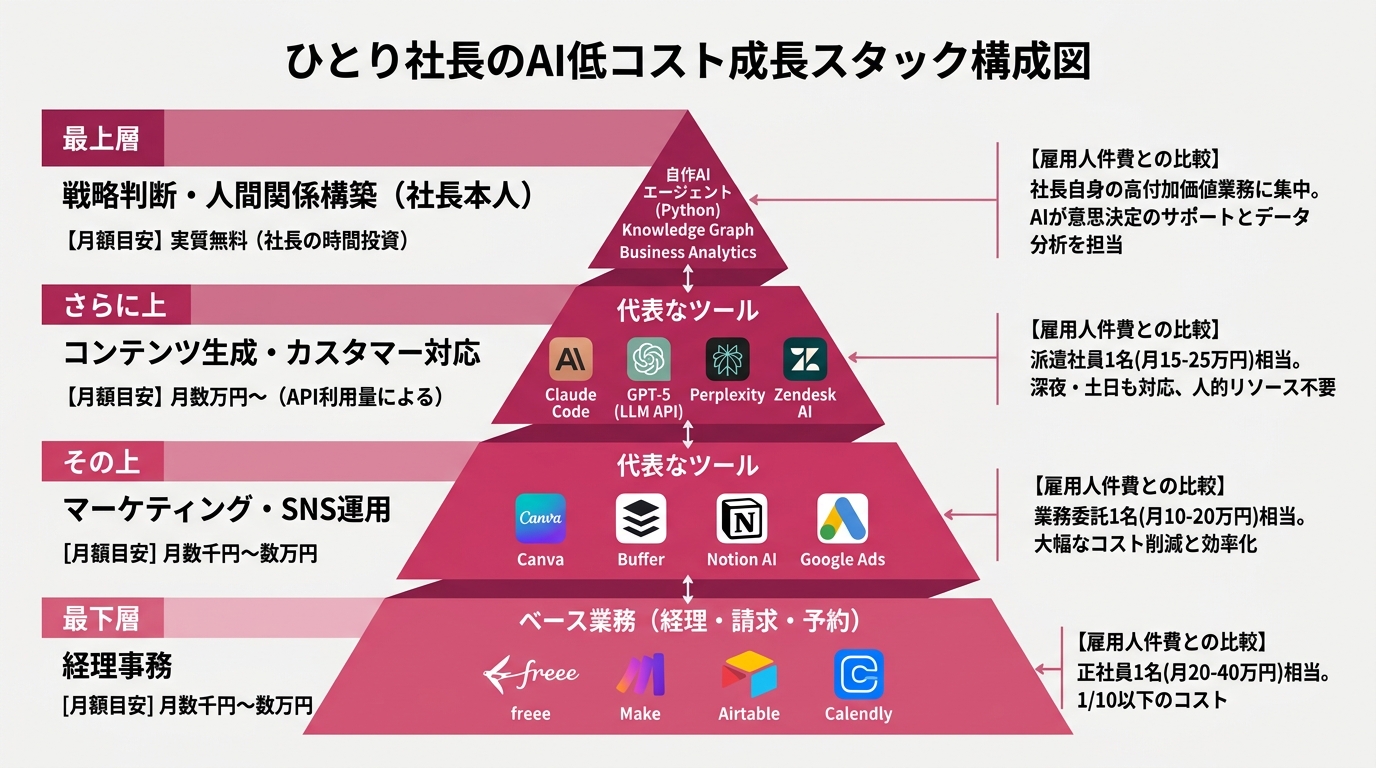

Weapon 3: AI low-cost growth. The economics of one person running “one company’s worth”

The third weapon isn’t about borrowing money. It’s about creating a state where you “don’t need to borrow.”

This is the biggest tectonic shift of 2026.

According to Professor Strebulaev’s research featured by Crunchbase, the typical time to unicorn status is about 6.6 years (10-year average). But in Q1 2026 alone, 47 companies leveled up from early stage (seed–Series B equivalent) to unicorn status — the largest cohort ever. Why is this possible? Because “letting AI handle it” is cheaper and faster than “hiring people.”

Accounting: With freee’s MCP integration, automate receipt scanning, journal entries, and tax filing drafts. Hiring someone costs ¥150K/month. AI runs $30–$50/month.

Marketing: SNS operations, blog writing, email distribution. Hiring costs ¥300K+/month. AI plus template design runs $50–$100/month.

Customer support: Auto-reply for inquiries, FAQ maintenance, in-Slack chatbots. Hiring costs ¥200K+/month. AI runs $30–$80/month.

That’s ¥700K worth of monthly work running on ¥20K–¥30K of AI spend. That’s the true source of the economics behind “one person running one company’s worth.”

Don’t misread this as “AI solves everything.” What AI can’t take over is strategic judgment and relationship building. First meetings with clients, long-term contract negotiations, crisis response. Without a human stepping in, the conversation never starts. That’s exactly why you need a design that “hands the base to AI so the human concentrates time on the most important work.”

I covered the case studies in detail in m2026042700011301 (Polsia ¥670M, Medvi ¥60B, Levelsio ¥450M). Polsia: solo founder, ¥670M-equivalent annual revenue. Levelsio: solo founder, ¥450M-equivalent across multiple businesses. Symbolic figures of the era of “solo founders reaching $M scale.”

If you thought “this is too early for me,” you’re wrong. You can start with $30/month in tool costs. There’s no early or late. Start today, and today’s worth of efficiency stacks up.

The combination blueprint for the three axes. Which one, in what order

After reading this far, you’re probably wondering, “Okay, I get the three axes, but how do I combine them?”

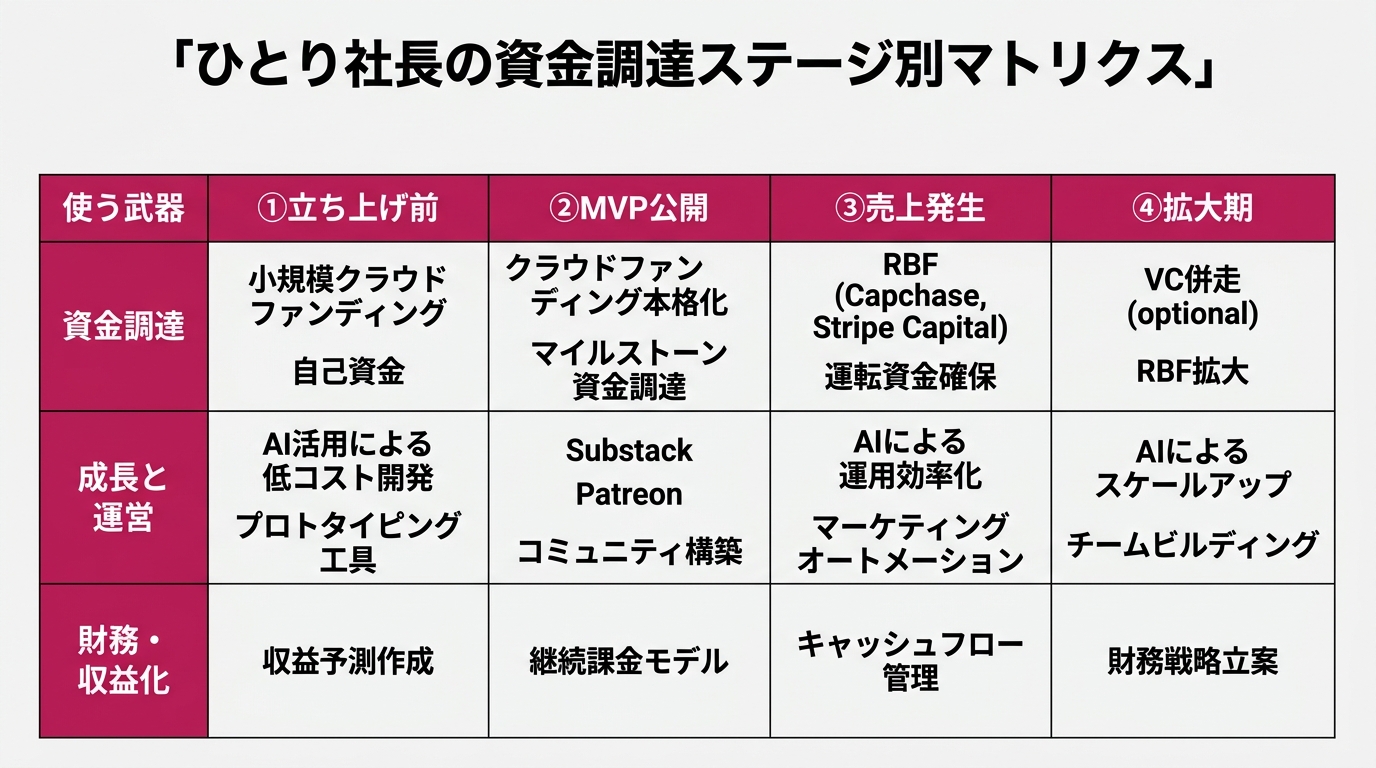

My recommendation: decide the stacking order by stage.

Phase 1 (pre-launch): AI low-cost growth + small-scale crowdfunding. You don’t need big money here. The right move is “set up your operations with AI before borrowing money.” Build your operational base with a few tens of thousands of yen in AI tools, then gather a small initial customer base via Substack, Patreon, or Buy Me a Coffee. Create the state of “100 supporters.”

Phase 2 (MVP release): Full crowdfunding + pre-sales. Here’s where you need your first chunk of capital. Go after the first 100 contracts. Indiegogo, Kickstarter, Substack, your own pre-sale — any of them work. Acquire “100 people who’ll pay upfront.” That becomes the collateral for the next phase.

Phase 3 (revenue generation): RBF (Capchase, Stripe Capital, etc.) + AI continuation. Once revenue starts coming in, RBF becomes a realistic option. Once monthly revenue evidence accumulates, Capchase clears underwriting in days. You can stretch cash 2–3x while keeping your cap table simple.

Phase 4 (expansion): If needed, run VCs in parallel or expand RBF. Only after reaching here does “the option of bringing in VCs” become “an option you choose yourself.” You don’t go meet VCs — you stand on the side where VCs reach out to you. And you can still decide not to take it. Reaching the soonicorn range of $500M–$999M without giving up equity is a realistic option now.

The order matters. Not “RBF out of the gate,” not “CF out of the gate.” Build operations with AI, gather customers with CF, accelerate growth with RBF. When the three axes interconnect, the synergy kicks in.

The first three moves. Implementation steps to start next month

Move 1: Build your AI setup in one week. Automate accounting with freee MCP. Write operational scripts in Claude Code or Cursor. Run SNS operations through Buffer or Later plus AI text generation. Monthly spend: $50–$200. With just this, you’re operating at the equivalent of ¥500K–¥1M/month worth of hired help.

Move 2: Get your customer list to 100 people in 30 days. Substack or a regular email list — either works. Build “100 people who’ll read it first.” Not SNS follower count — the count of “people who handed you their email address.” With 100 people, the next phase’s pre-sale takes off. With zero, it doesn’t. The gap is decisive.

Move 3: Start either pre-sales or RBF registration. If you have zero revenue, start with pre-sales. Sell your annual plan as “50% off for the first 100 customers.” A ¥100K annual plan at ¥50K × 30 customers = ¥1.5M cash. That alone is 3 months of working capital. If you already have $5K+/month in revenue, wait for a Stripe Capital notification or register with Capchase. RBF underwriting looks at payment data, not financial statements, so you don’t waste time assembling Excel paperwork.

You don’t have to do all three moves. Just one, and you’re in motion.

Don’t flinch at “starting next month.” “Think while moving” is my baseline. Better results come from running and correcting mid-stride than from a perfect plan. I’ve proven this many times since going independent.

Wrap-up. How to walk in the era of reaching the goal with zero VC meetings

2026 is the year “fundraising without relying on VCs” became a realistic option. Allied Market Research projects the RBF market will balloon from $9.77B in 2025 to $15.86B in 2026. The Crunchbase Q1 tally shows 80% of capital concentrated in AI, and the cost of launching a solo-founder business has dropped to one-tenth of what it was a few years ago.

What I wanted to convey today is one thing. To people who say, “I don’t have connections to meet VCs, but I want to reach the goal,” I want to hand over a three-axis map.

- Weapon 1: RBF — Don’t give up equity, repay with a slice of monthly revenue

- Weapon 2: Crowdfunding — Customers become prepaying investors

- Weapon 3: AI low-cost growth — Economics of one person running one company’s worth

Stack the three axes in order, and the path to the $500M–$999M soonicorn range with zero VC meetings genuinely exists. I haven’t tried every path myself. But almost everyone I see succeeding around me is using one of these three axes. Giving up because “I have no VC connections” is a 2020 mindset.

Of today’s three moves (AI setup, customer list of 100, pre-sale or RBF registration), pick one and start it this week. Once you’re in motion, I’ll write the rest.

“In the end, the ones who actually do it win.” That’s the entirety of my action principle.

Sources

- Allied Market Research “Revenue-Based Financing Market” (published 2024): $6.4B in 2023 to $178.3B by 2033, 39.4% CAGR

- Research and Markets “Revenue-Based Financing Market Report 2026”: $9.77B in 2025 to $15.86B in 2026

- Crestmont Capital “Revenue-Based Financing Statistics”: North America 60%, user base distribution

- Crunchbase News “Q1 2026 Record Breaking Funding”: Q1 $300B, AI 80%

- Crunchbase News “Unicorn Formation Timeline”: 6.6 years to unicorn, 47 early-stage companies in Q1

- Kickstarter Official Statistics Page: $8B+ cumulative pledges, 600,000+ projects

女性だからこそ、AIを使いこなさなきゃって思ってる。仕事も、副業も、推し活も、旅行も、全部やりたい。人生一度きりなのに時間は足りないじゃん?だからAIに任せられることは全部任せる。浮いた時間で本当にやりたいことをやる。それがあたしのスタイル。ここにはあたしが実際にやったことをまとめてるだけ。誰かのためになったらいいなって思って書いてるよ。