Chinese Cities Are Throwing $1.4M Subsidies to Steal AI Solo Founders. US is Bottom-Up, China is State-Driven, and Here Are 3 Questions for Squeezed Japanese Solos to Reset the Game Right Now

China's local governments have started mass-producing 'AI solo founders' with subsidies. With a different game now running alongside the US bottom-up unicorn model, here are 3 questions Japanese solo CEOs need to ask to reset how they fight.

What you'll learn in this article

- The key point to grasp before reading the full article

- How the issue changes practical decisions after reading

- Which follow-up article is worth opening next

In March, the Shangcheng District of Hangzhou announced a plan aimed at solo founders. Build out 10 dedicated communities within 2026, attract 1,000 AI solo founders, nurture 100 AI companies. The whole picture, assembled in one shot (Chinese state-run English media chinadaily.com.cn regional edition, March 17, 2026).

Just looking at the numbers, the scale is abnormal. And it’s not just Shangcheng District.

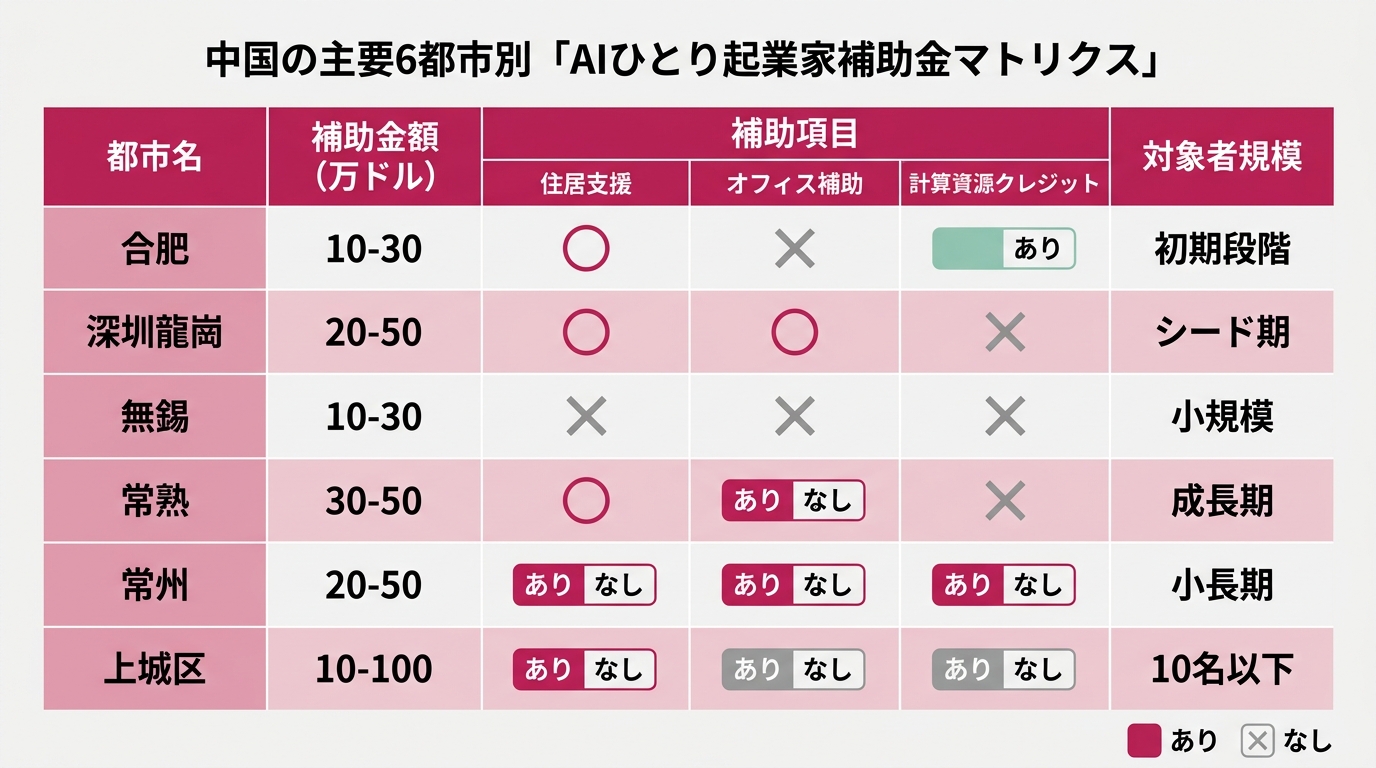

Hefei (Anhui Province) and Shenzhen’s Longgang (Guangdong Province) have set up support packages including housing, office space, and computing resources, with subsidies worth up to $1.4 million per team (about ¥210 million). Wuxi offers about $700,000, Changshu about $830,000. Changzhou puts up around $700,000 plus an additional $280,000 for computing resources. Source: Rest of World’s roundup article from 2026-03-18.

Writing this article, I honestly thought, “they got us.”

“Solo CEOs” and “solopreneurs” (people running businesses by themselves) have been the lead characters in my articles for the past year. I’ve covered bottom-up American solo founders like Polsia, Medvi, and Levelsio. I delivered them with the message “we Japanese can do this too.”

But now, a different route has emerged. China is running a system where the central and local governments stack subsidies to “mass-produce” solo CEOs. The US is bottom-up, China is state-driven. The map of AI solo entrepreneurship has changed structurally.

This article does three things. ① Lay out all the Chinese numbers. ② Compare the US “bottom-up” and Chinese “state-driven” structures. ③ Three questions Japanese solos need to reset right now. After reading, I want you to redraw your own combat map once. Without redrawing the map itself, you’ll be paralyzed in the pincer between bottom-up and state-driven.

First, Let’s Lay Out All the “Numbers” Chinese Cities Are Moving

Just facts first. Opinions later.

Hangzhou’s Shangcheng District (chinadaily.com.cn 2026-03-17) plan goes like this:

- 10 dedicated solo CEO communities to be built within 2026

- Nurture 100 AI-related companies

- Bring 1,000 entrepreneurs into the district

- Provide over 20,000 square meters of move-in-ready office space

- Subsidize workstations for up to 3 years

- Housing support at designated apartments and talent hostels included

Hefei is the capital of Anhui Province. Within China, it’s known as a cluster for AI and semiconductor industries. Its tech district provides solo CEO teams with packages including housing, offices, and computing resources. Worth up to $1.4 million (about ¥210 million) (Rest of World).

Shenzhen’s Longgang District also has the same up-to-$1.4M tier. Shenzhen has long been the heart of tech. Longgang is reportedly running an AI support program for solo CEOs, which English media call “OpenClaw” (The Decoder, March 2026. The name in primary Chinese government documents has not been confirmed).

Three cities in Jiangsu Province are a bit smaller. Wuxi offers about $700,000 plus computing resource credits (prepaid quotas usable for cloud services). Changshu offers about $830,000. Changzhou’s tier is about $700,000 plus a separate $280,000 for computing resources. All three cities also offer service subsidies in the form of “3 years of free office space” on top of the cash subsidies.

Looking at Shangcheng District’s plan in detail, it commits to providing over 20,000 square meters of office space. With a 3-year occupancy subsidy. And the government even arranges housing called “talent hostels.” Rent is subsidized in tiers by income level.

What about totals? Rest of World writes “thousands of companies.” Caixin Global headlined “China bets on AI solo CEOs to lift employment” (2026-02-14). Xinhua shifted its phrasing. “Building an ecosystem to nurture AI super-individuals” (Xinhua 2026-04-23 English edition).

Even People’s Daily English edition moved. They ran a feature: “AI tools spread Chinese solo CEOs” (People’s Daily 2026-02-05). The fact that Chinese state-run media chose “solo CEOs” as a marquee theme is heavy. That’s how policy intent surfaces.

Lining all of this up, what I feel is the “scale” and the “all-out war” vibe. It’s not that one company or one local government is sticking out. Multiple cities and multiple regions are moving simultaneously. That’s why I thought “they got us.”

Why the US “Bottom-Up” and the Chinese “State-Driven” Are So Different

Next, I’ll compare structures. What’s actually different between the US and China.

In the US, the lead role for solo CEOs is the “bottom-up” type, picked up by venture capital (VC, equity investors). Look at Carta’s (an equity management platform) 2026 data. In the first half of 2025, 36.3% of newly founded startups were by single founders. In 2024, it was about 30% (Carta Founder Ownership Report). Nearly doubled in 10 years.

The poster children are the 5 cases of Polsia, Medvi, and Levelsio I wrote about last week. Polsia: $4.5M annual recurring revenue (ARR, sales that come in continuously every year), funded by True Venture. Medvi was sold to Wix for about $80M, ranking alongside the Base44 first-year hit case. Levelsio is the independent type who started from a $30K/month café-coworking lifestyle.

What they share: “individuals can now carry the functions of a company alone with AI.” Same premise as Anthropic’s Dario Amodei saying there’s a 70-80% chance of a one-person unicorn within 2026. What’s different is “who” lifts up that individual and “how.”

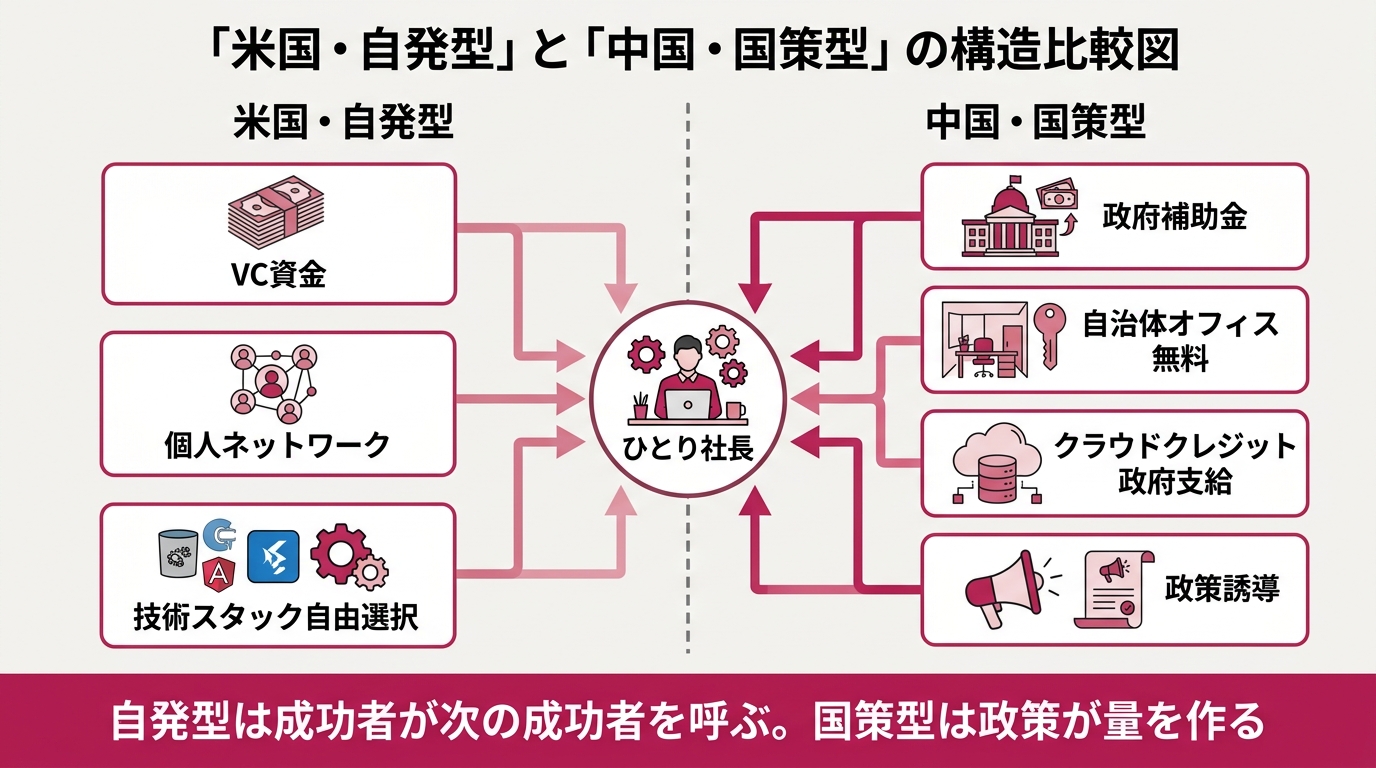

The bottom-up type (US) has 3 traits.

- Mechanisms exist for VC investors to discover individuals

- SNS posting is the front gate for personal brand

- Tech stacks (the combination of AI tools and services used) are completely free to choose

The substance is a “successful person calls the next successful person” chain reaction. The fact that Pieter Levels built Levelsio and succeeded moves the next thousands.

The state-driven type (China) also has 3 traits.

- The government uses subsidies to push entry costs near zero

- State media intentionally mass-produces “success cases”

- “Encouraged industries” are presented up-front by policy

Karen Dai runs SoloNest, based in Shanghai. She’s in the position of holding weekend events for solo entrepreneurs. She told the Japan Times: “It used to be very hard to run a business by yourself. AI broadened the range of tasks it can help with, and barriers to entry came down” (Japan Times 2026-04-22).

This is a comment symbolic of the AI era. The same can be said in Japan and the US. What’s different is that China built this “barrier reduction” into employment policy at the national level.

“Bottom-up moves people with success. State-driven manufactures volume with policy.” That’s the fundamental structural difference. We’ve been listening only to the bottom-up story and running with it. With China’s state-driven model now in motion, we need to realize half the map was invisible to us.

Why Did China Have to Move with State Policy?

If you only look at the numbers, it sounds like “China is strong.” But reading the background reveals more urgent motives.

First, high youth unemployment. According to the Japan Times, in China, 1 in 6 young people aged 16-24 doesn’t have a job. This is a state of “the energetic generation can’t move.” It breeds social instability.

Second, the workplace practice known as “35-year-old retirement.” It’s reported that at many Chinese IT companies, employees over 35 are effectively forced into early retirement (Japan Times). To Japanese sensibilities, it’s an even harsher version of the “45-year-old retirement debate.” Where do 35-year-old engineers go in a society that demands their resignation?

Third, Beijing’s “tech self-reliance” policy. Building a domestic AI ecosystem that doesn’t depend on the US is a national goal. “Mass-produce 1,000 solo entrepreneurs in one district” fits into this. Rather than competing with giant IT companies through one big firm, the picture is for 1,000 small individuals to spread out and support the ecosystem.

One concrete example. Wang Tianyi, a 26-year-old former product manager. He left a Chinese internet company last year and started solo production of AI-generated commercials. Now earns up to ¥40,000 RMB ($5,800, about ¥870,000) a month. He told the Japan Times: “Solo CEOs will become a major trend going forward.”

Whether you see Wang Tianyi’s monthly income and think “amazing” or “normal in Japan too,” set that aside. What matters is that he calculated “the risk of staying an employee” and decided “the risk of becoming a solo CEO” was smaller. This is happening simultaneously across China.

The Chinese government “boosts them with subsidies.” For these individuals, it’s a hedge against unemployment risk. For the government, it’s a cheap response to the employment problem. Both interests align.

In my 4/25 article, I covered the topic that “the average age of AI entrepreneurs is dropping sharply from 40.” China’s current move is on the extension line of that article. Globally, “young individuals moving small and fast” is happening, and China accelerated it with policy.

In other words, China is also covering its “weakness” with state policy. Without understanding this, you end up with an impression that ends at “China is strong.”

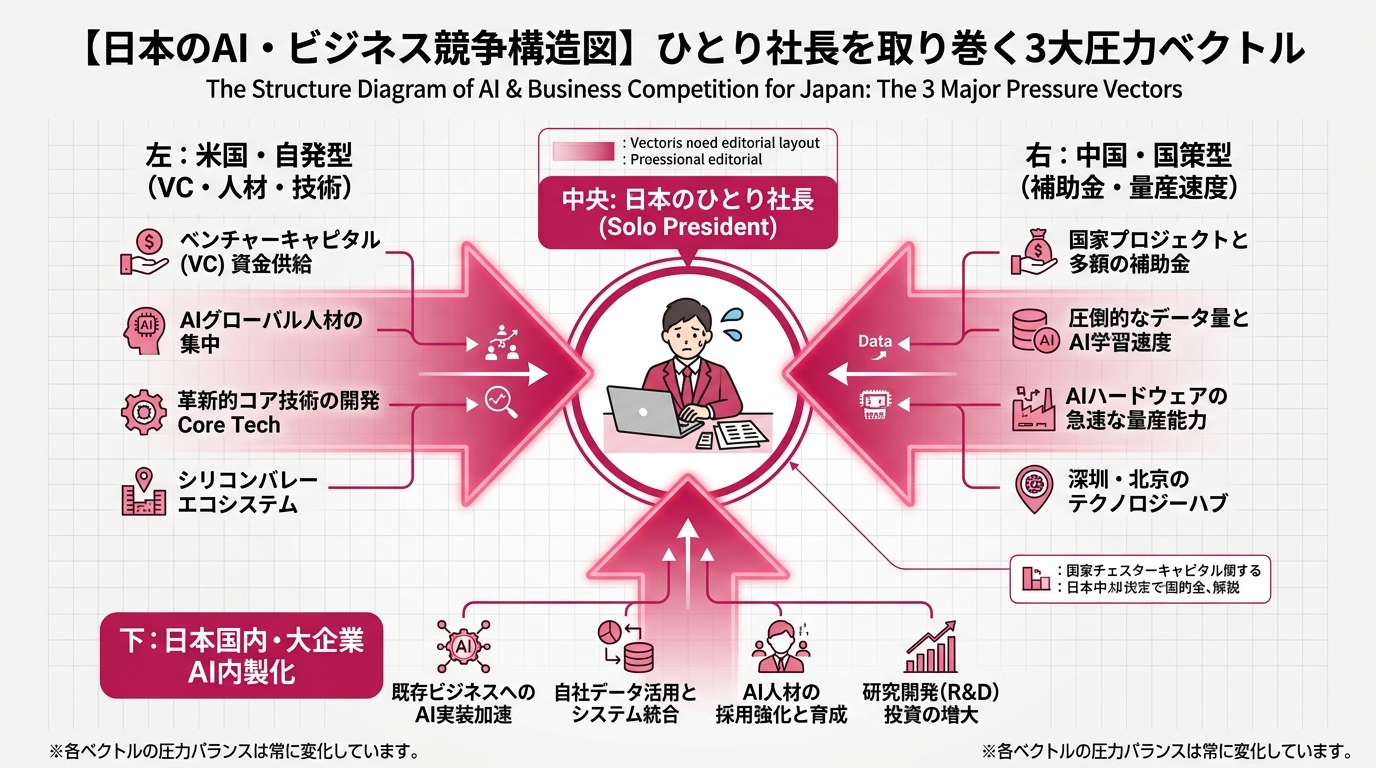

Japanese Solo CEOs Are Now Being Squeezed from 3 Directions

Here’s the main point. What about us in Japan?

Honestly, Japanese solo CEOs are now squeezed from 3 directions.

First direction, the US bottom-up. VC money, global talent, the latest tech stacks—all assembled. If you’re going to win the world with an AI startup, the US is still the favorite. If we Japanese try to follow the US playbook, we’ll almost certainly fall behind.

Second direction, the Chinese state-driven. As we just saw. If individuals subsidized with ¥210 million go up against us self-funded folks on the same arena, we can’t win on cost structure. Going after the Chinese domestic market isn’t realistic. But—if AI services commoditize globally, the story changes. Commoditization means differentiation gets hard and you fall into price wars. The wave of price collapse hits us in Japan too.

Third direction, in-house AI build-out by Japanese big enterprises. Distribution of Claude Code to all engineers and acceleration of AI training for business roles are happening one after another at Japanese IT companies. Until now, “small/mid companies wanting AI efficiency” were a chunk of solo CEO customers. Some portion of that starts being replaced by big enterprises’ in-house AI.

Squeezed from 3 directions, how do we move?

First, admit the fact that we can’t win on “simple price competition,” “simple feature competition,” or “simple information-volume competition.” Try to fight on price against China’s ¥210M subsidy and you collapse. Try to fight on feature count against US VC-backed startups and you lose on dev resources. Try to fight on information volume against Japanese big enterprises’ in-house AI and you’re disadvantaged on infosec.

So what do we win on? That’s the next section.

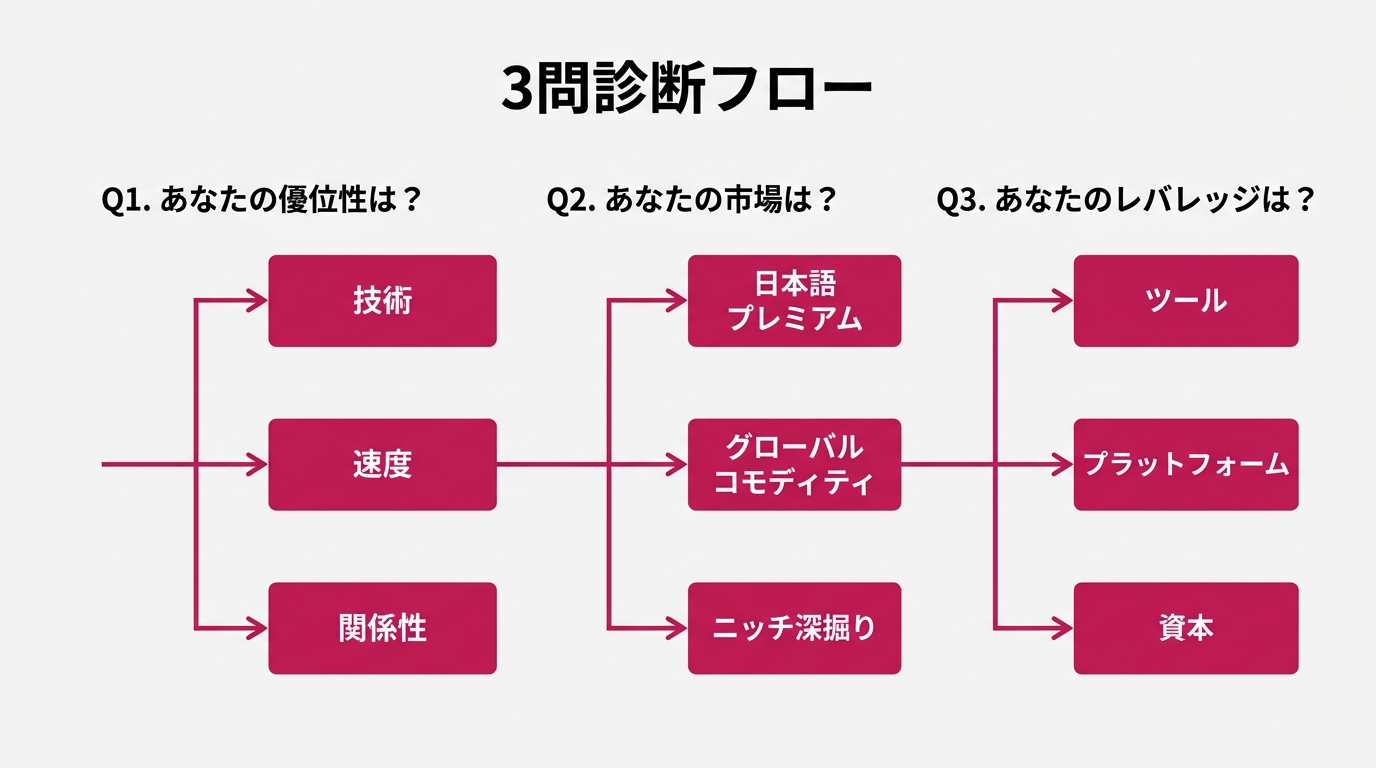

3 Questions to Reset the Competitive Environment. With My Own Answers

I’ll share the 3 questions I’m asking myself right now. Write your own answers as you read.

Question 1: Is my edge “tech,” “speed,” or “relationships”?

Compete on tech and you approach the US model. Compete on speed and you can’t beat China’s mass-production speed, but you can beat Japanese big-enterprise decision speed. Compete on relationships and Japanese-language context, industry customs, and existing trust become weapons.

My answer is “relationships.” Almost 100% of my consulting contracts come from referrals and existing relationships. I’m not selling tech or speed. The relationship of “I want this person specifically” is the primary contract source. This is an asset that can’t be replicated by Chinese subsidies or US VC.

Question 2: Is my market “Japanese-language premium,” “global commodity,” or “niche depth”?

The Japanese-language premium market is the territory only deliverable by people who understand Japanese context and Japanese industry customs. The global commodity market means deploying in English and taking customers from around the world, but exposing yourself to price competition. The niche-depth zone is narrowing down to specific industries and specific challenges and competing on depth.

My answer is “Japanese-language premium + niche depth hybrid.” Specialized in Japanese SNS marketing, narrowed within that to “solo CEOs and SMB owners.” People moving on Chinese subsidies don’t come to Japanese niches. US VC-backed companies tend to defer the Japanese market. Going to a place where you’re not squeezed.

Question 3: Is my leverage “tools,” “platforms,” or “capital”? Leverage is a mechanism that produces big results from small personal effort.

Tools are AI. Platforms are SNS and communities. Capital is subsidies and self-funding.

My answer is “platforms + tools.” SNS and communities are the primary customer-acquisition device, and AI is the sub-device for ops efficiency. Capital is intentionally minimized. The Chinese model is built to compete on capital (subsidies). The US model is also designed to compete on capital (VC). I gave up the path of competing on capital from the start.

Answer all 3 questions and you have a one-page strategy map. Continue as a solo CEO without writing this and you’ll be fighting on the opponent’s arena. Now that Chinese subsidies are in motion, it’s time to redraw the whole map.

Summary. China’s Move Isn’t a Threat—It’s a Trigger to Redraw the Map

The fact that China started state-driven mass production of AI solo entrepreneurs is not a threat to us in Japan. That’s what I think.

If anything’s a threat, it’s the trap of believing we can keep fighting the way we are now. What’s scarier is staying still while building your strategy referencing only the US VC model.

Looking at China’s move, the AI solo entrepreneurship map has at least 3 routes.

- The US bottom-up (VC, free market, success chain)

- The Chinese state-driven (subsidies, policy steering, mass-production speed)

- The route for us Japanese (no name yet)

We ourselves are the ones drawing the third route. Wait for someone to define it for you, and you’ll end in the pincer of bottom-up and state-driven.

Three things I want you to do this week.

- Actually read the relevant articles in Rest of World and Japan Times (build the habit of going to primary sources)

- Write your edge, market, and leverage on paper as answers to the 3 questions

- Determine whether your answers lean “bottom-up,” “state-driven,” or “Japan-original”

I’m in the middle of rewriting my own answers right now. Looking at China’s move, I felt I needed to bring up the resolution of “niche depth” one more notch. There are still territories in specific Japanese industries that Chinese state policy doesn’t reach and US VC doesn’t pick up. I’m going there.

Reader, you also should re-read your own terrain. Think while moving, move while thinking. That’s the privilege of a solo CEO. Even squeezed from 3 directions, read the terrain and there’s always a way through. Let’s move.

女性だからこそ、AIを使いこなさなきゃって思ってる。仕事も、副業も、推し活も、旅行も、全部やりたい。人生一度きりなのに時間は足りないじゃん?だからAIに任せられることは全部任せる。浮いた時間で本当にやりたいことをやる。それがあたしのスタイル。ここにはあたしが実際にやったことをまとめてるだけ。誰かのためになったらいいなって思って書いてるよ。