How to Choose Marketing Tools Has Changed: What Ahrefs' Entry and the $1.9B Acquisition Reveal About 2026's 'Consolidation Phase'

Four months after Ahrefs entered social media management. Place it alongside Adobe's $1.9B Semrush acquisition, and you can see the martech market shifting from 'expansion' to 'consolidation.' Here's why the tool you pick today should be chosen on the assumption that the entire map will change in six months.

What you'll learn in this article

- The key point to grasp before reading the full article

- How the issue changes practical decisions after reading

- Which follow-up article is worth opening next

“Another tool got consolidated?”

That’s the phrase I’ve heard most often from marketers on Zoom this past month. It’s been four months since Ahrefs Social Media Manager launched. Adobe acquired Semrush for $1.9 billion, and Hootsuite has been beefing up its AI features. It looks like a string of one-off feature releases on the surface, but if you watch carefully, something else is going on.

In yesterday’s article, I shared a framework for deciding “can I remove one tool from my own stack?” Today is the follow-up — a macro view of how “the market as a whole is moving to reduce tools.”

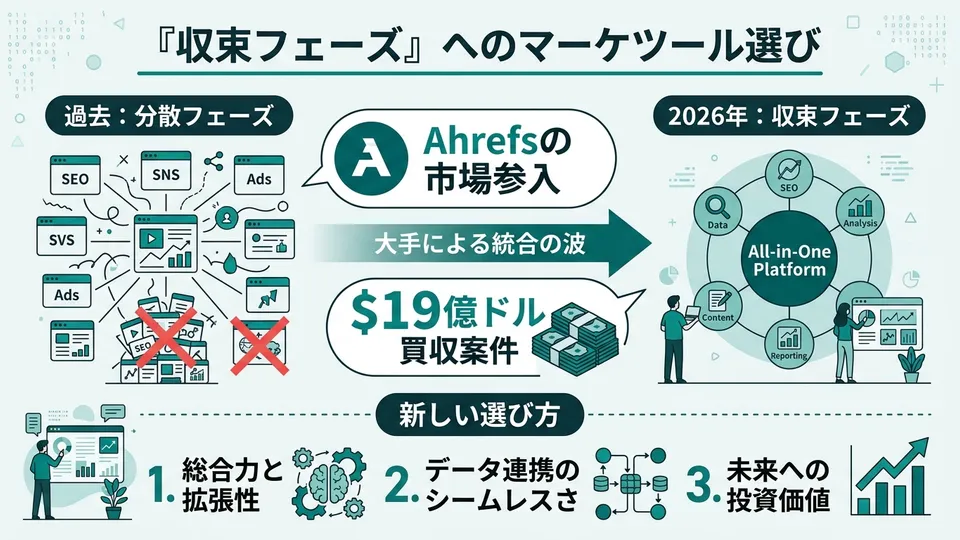

Let me start with the conclusion. The way I see it, the martech market entered 2026 and started moving from an “expansion phase” toward a “consolidation phase.” Ahrefs entering social isn’t an isolated event — it’s part of a market reshuffle happening in parallel with Adobe’s Semrush acquisition. If you’re stuck on a tool decision right now, you need to rebuild your decision criteria on the assumption that “the entire map will change in six months.”

What Has Moved in the Four Months Since Ahrefs Entered — A Timeline of the Martech Market

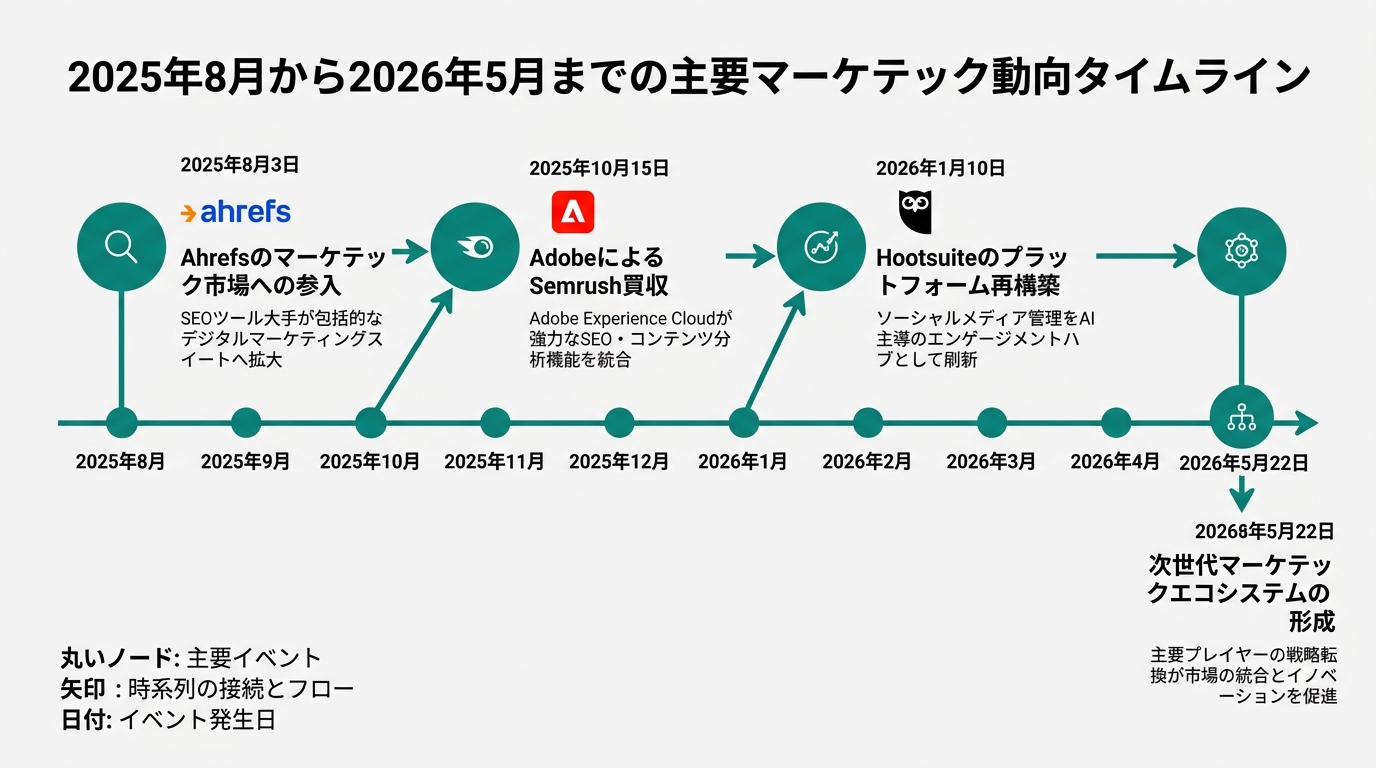

First, let’s build a timeline of what’s happened in the four months from the Ahrefs entry breakdown I wrote on 3/30 to today.

| When | Event | Category |

|---|---|---|

| August 2025 | Ahrefs CMO Tim Soulo announces early access to social media management features on X | Consolidation begins |

| November 2025 | Adobe announces $1.9 billion acquisition of Semrush | Major consolidation |

| January 22, 2026 | Ahrefs Social Media Manager officially launches on Japanese site (PR TIMES) | Consolidation accelerates |

| April 2026 | Hootsuite restructures AI generation and analytics features “OwlyGPT” as an integrated experience | Feature reorganization |

| May 2026 | Buffer and Sprout Social continue their strategy of narrowing into specific domains | Niche specialization |

Line them up and you can see five news items in just nine months. “Five major reshuffles in nine months” in the martech industry is clearly an abnormal pace compared to recent years.

What’s worth noting here is that these aren’t independent events. Right after the Semrush acquisition announcement in November 2025, Ahrefs accelerated its move from early access to full release. Sprout Social tightening its focus on customer support integration is also a choice to avoid head-on competition with consolidated players.

In other words, we’ve entered a stage where “one company moves, three companies react.” This is the classic pattern of a consolidation phase.

If you look at the timing of the entries and acquisitions from another angle, another pattern emerges. Ahrefs is on the “expand features starting from SEO” track. Adobe bought Semrush to “absorb SEO starting from content.” Both are trying to swallow adjacent territory starting from their core strength. That’s the real shape of the major moves of these four months.

The Meaning of “$1.9 Billion” — The Adobe Semrush Acquisition Was the Foreshadowing for Ahrefs’ Entry

If you only hear the Ahrefs entry story, it’s easy to land on “huh, an SEO tool started doing social management.” The moment you place the Adobe Semrush acquisition alongside it, the view changes.

In November 2025, Adobe announced it would acquire Semrush for a total of $1.9 billion (about ¥280 billion) (Adobe Newsroom announcement, November 13, 2025). Semrush is an 18-year-old SEO and content marketing platform. Adobe’s purpose in absorbing it: “to deliver content from discovery to engagement end-to-end.”

Let’s compare that $1.9 billion figure to another acquisition.

- Adobe Semrush acquisition: $1.9 billion (2025)

- Salesforce’s acquisition of ExactTarget (the canonical example of a major marketing automation consolidation): $2.5 billion (2013)

Place these two side by side and you can see that $1.9 billion is “a rare scale even in past marketing consolidation history.” This is not a small story.

“Adobe came in seriously to claim the SEO domain.” The moment that signal went out, Ahrefs must have faced two choices. One was to stay specialized as an SEO tool. The other was to step into adjacent domains and offer a different shape of integration from Adobe’s. Ahrefs chose the latter. It started early access to social media management features in August 2025 and officially launched in January 2026. The timing is right after the “Adobe Semrush acquisition announcement.”

In my honest report after four months of use, I wrote that “Ahrefs Social Media Manager isn’t winning on feature count.” Even so, the reason Ahrefs rushed wasn’t a question of feature superiority — it was a strategic necessity of “becoming a consolidation player in the marketing stack.”

What you can read here is the essence of Ahrefs’ move. It’s not “an SEO tool adding new features.” It’s a declaration of expansion: “become a major player in the martech market.” Once you see that, the recent moves of Buffer, Hootsuite, and Sprout Social start to make sense too.

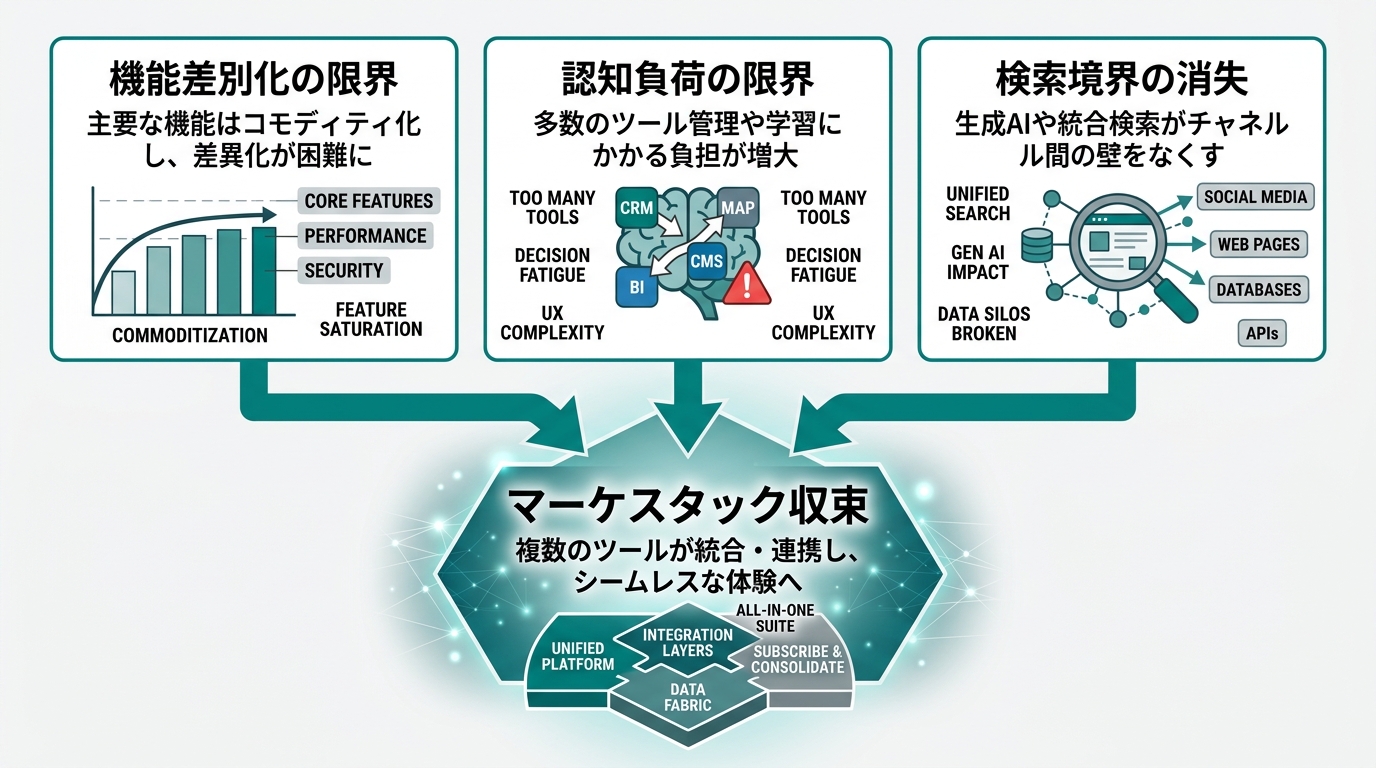

Why We’ve Entered the Consolidation Phase Now — Three Structural Drivers

The phenomenon of “tools getting consolidated” always has structural reasons. Let me lay out three reasons why this movement is concentrated in martech in 2026.

Driver 1: AI generation costs have plummeted, and feature differentiation no longer works

From 2024 through 2025, generative AI token costs dropped sharply. Across the major models from Anthropic, OpenAI, and Google, pricing per 1M output tokens is at a fraction of what it was a few years ago. What this means: feature gaps are disappearing. Post idea generation, keyword clustering, article draft generation — we’ve entered an era where any tool can implement these at the same level.

When you can’t differentiate on features, a tool’s strength becomes “breadth of data” and “degree of workflow integration.” Ahrefs’ backlink database, Adobe’s ad delivery data, Semrush’s search keyword history. These can only be obtained through acquisitions or long-term investment. So the competition has shifted from features to “data integration.”

Driver 2: Marketer cognitive load has hit its limit

Many of the marketers I’ve talked to have the complaint that “there are too many tools, I can’t keep up with management.” It’s not unusual to hear that login credentials have grown past ten, and the morning is gone just from bouncing between dashboards. Even in the marketing map cleanup I covered in the 4/24 article, many people had tools they “couldn’t even keep track of.”

The more tools you add, the more logins, notifications, and dashboards you accumulate, and the less time you have for decisions. The whole industry has reached the tipping point where “adding tools” lowers productivity. When buyers start saying “we don’t want any more,” sellers have no choice but to build “everything-included” consolidated platforms.

Driver 3: The boundary between AI search and social search has disappeared

Use of generative AI search like ChatGPT, Perplexity, and Gemini is expanding. Sprout Social’s 2025 Q2 survey produced a surprising number (Sprout Social official press release, surveying 2,280 people in the US, UK, and Australia). 41% of Gen Z use social media as a substitute for search engines. The basis for operating “Google, social, and AI search” as separate domains is disappearing.

When the era of tools split along that “boundary” ends, the tools themselves have to consolidate too. This is the real meaning of Ahrefs Social Media Manager. It presented “tool design after the boundary disappeared” to the market.

The three drivers look independent, but they reinforce each other. That’s why the wave of consolidation is this concentrated in 2026.

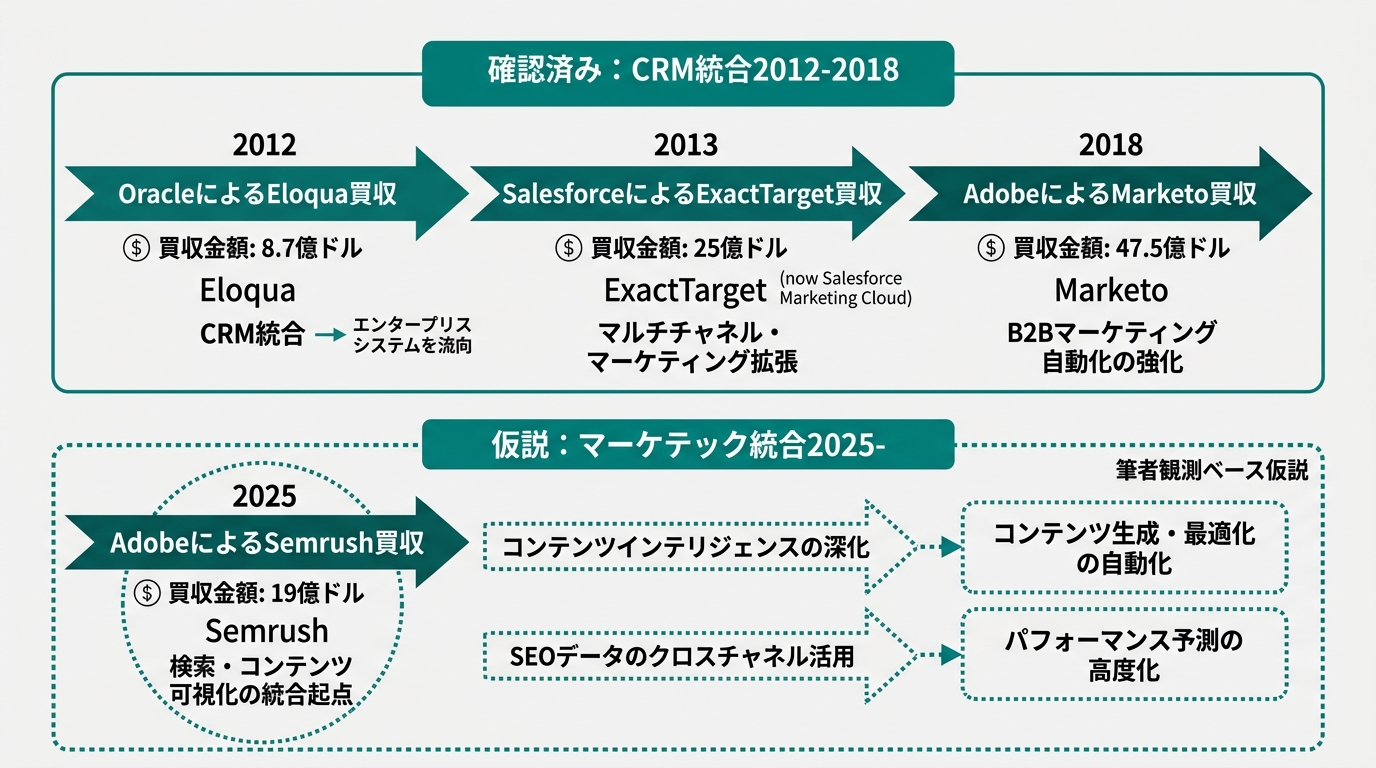

Learning Consolidation Patterns from Past Cases — Lessons from CRM Consolidation (2010s)

When thinking about “what happens next,” past consolidation phases with similar structures are useful references. The closest analog to martech is the CRM and marketing automation consolidation history of the 2010s.

Around 2010, each tool stood independently. CRM was Salesforce; marketing automation was Eloqua, Marketo, and HubSpot. Marketers at the time took it for granted that “CRM and MA are separate tools.”

Then between 2013 and 2015, here’s what happened.

- 2012: Oracle acquires Eloqua for $870 million

- 2013: Salesforce acquires ExactTarget for $2.5 billion

- 2018: Adobe acquires Marketo for $4.75 billion

A major acquisition every 3–5 years, and by around 2020, “CRM, MA, and email delivery integrated into one platform” became normal. The reason HubSpot survived as an independent player is that it aimed at “all-in-one” from the start.

Let me distill three lessons from this CRM consolidation history.

First, if the CRM consolidation analogy holds, the consolidation phase calculates out to a 3–5 year completion. It’s six years from the first major acquisition in 2012 to the Marketo acquisition in 2018. During that period, independent players split into “get acquired,” “niche down into a specialized domain,” or “become all-in-one.” Tools stuck in the middle almost all disappeared.

Second, buyers invested in consolidation against the opinion that “the independents are good enough.” At the time of 2013, there was internal debate among marketers over “isn’t ExactTarget fine as an email delivery tool?” Even so, Salesforce paid $2.5 billion to buy it. The reason was the long-term strategy that “integrated data drives more upsell.” Adobe’s motivation to pay $1.9 billion for Semrush in the martech domain is structurally the same.

Third, the marketer’s job shifted from “tool selection” to “data integration design.” What the strong marketers of the late 2010s were thinking about wasn’t which CRM to pick. It was which MA to pass the data flowing out of the CRM to, and which attribution model to measure impact with. Tool-level selection became a peripheral problem.

Holding the hypothesis that martech consolidation might follow the same path in your head sharpens decision-making. Before agonizing over “Ahrefs or Buffer,” there’s something more important to think about. “How does my data flow, and where does it get used for decisions?” That question pays off more three years from now.

Three Positions Marketers Can Choose Now

The macro discussion has gone on long enough — let’s bring it down to your own work. In a martech market that has entered the consolidation phase, there are three positions marketers can choose right now.

Position 1: Ride the consolidation wave (consolidate into an integrated platform)

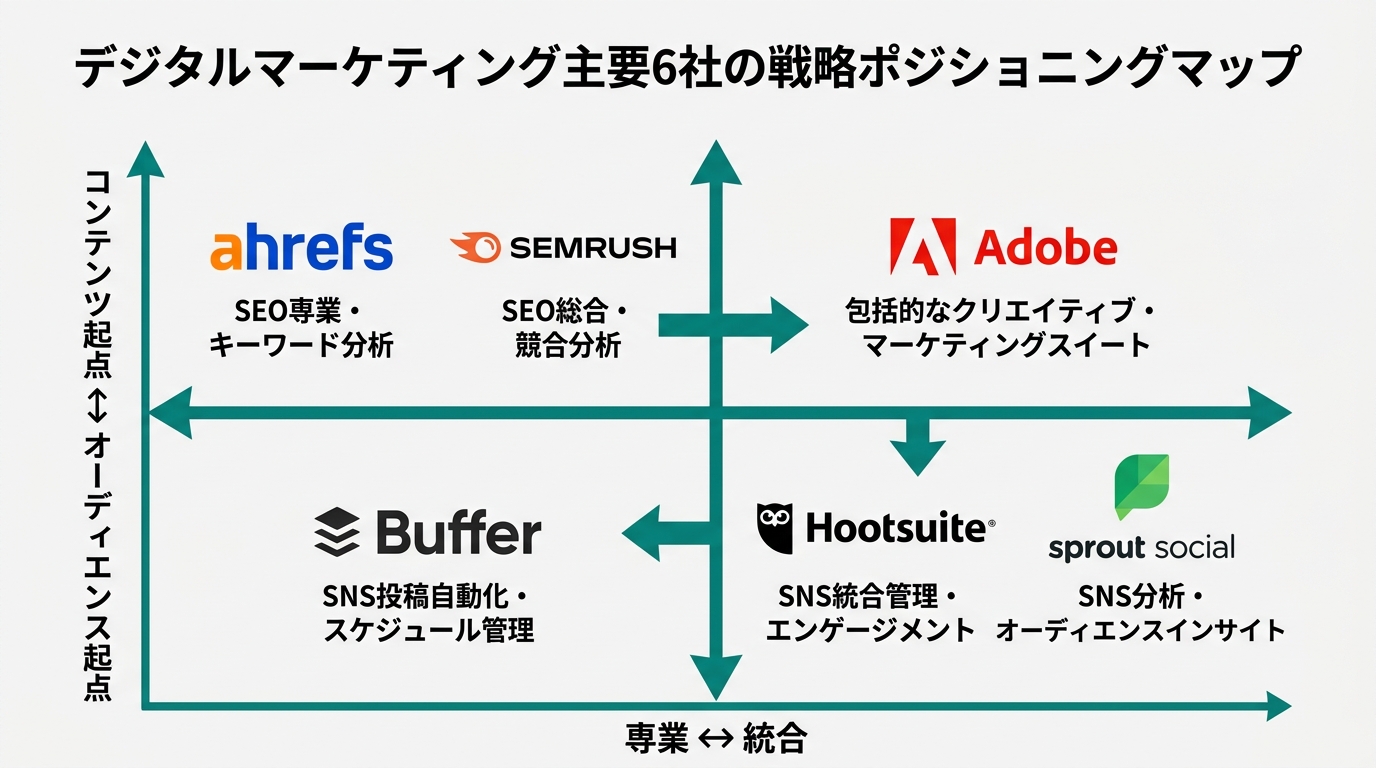

Build around Ahrefs to integrate SEO, social, and content. Or build around Adobe Experience Cloud (post-Semrush integration). That route bundles content and audience together. The thinking is to anchor your work onto one integrated platform.

The upside is faster decisions. When data sits in one place, reporting and strategy pivots move faster. The downside is lock-in risk. You can get whipsawed by the platform’s pricing changes or strategic pivots.

This fits “solo marketers,” “marketing leads at small and mid-sized companies,” and “people whose work has a strong need for data integration.” If you meet the three conditions from my previous four-month report for “people who can drop one tool,” this position should significantly boost your efficiency.

Position 2: Hold your own axis (niche down in a specialty domain)

The direction of intentionally picking specialized tools rather than riding an integrated platform. For example, keep Buffer for “the speed of its scheduling UI.” Keep Sprout Social for “customer support integration.” Keep SE Ranking for “cost optimization.” The approach is to keep choosing the best tool for each individual purpose.

The upside is best-in-class performance in each domain. The downside is that you have to handle the data integration between tools yourself. The load of being the connective tissue — Zapier, Make, spreadsheet linkages, API connections — falls on you.

This fits “agencies running multiple brands” and “specialists who demand high performance in a specific domain.” Agency work and professional services people get more out of this.

Position 3: Wait and see (decide again in six months)

“I can’t decide right now” is a legitimate choice. The martech market is going to move significantly over the next 12 months. How Adobe will move forward with the Semrush integration. What additional features Ahrefs will roll out. Whether Hootsuite ends up as the acquirer or the acquired. Sometimes moving after these become visible leads to the right choice.

But people who take this position need to decide “what to watch.” Three things I track: Ahrefs’ official roadmap, the progress of the Adobe x Semrush integration, and the monthly major martech news on PR TIMES. Following just these gives you a steady read on the pace of consolidation.

It’s not a question of which of the three positions is the right answer. You decide based on your work style and your need for data integration. Pick one position by running it through the previous decision framework, and revisit in six months. Just doing this is enough to tighten the decision.

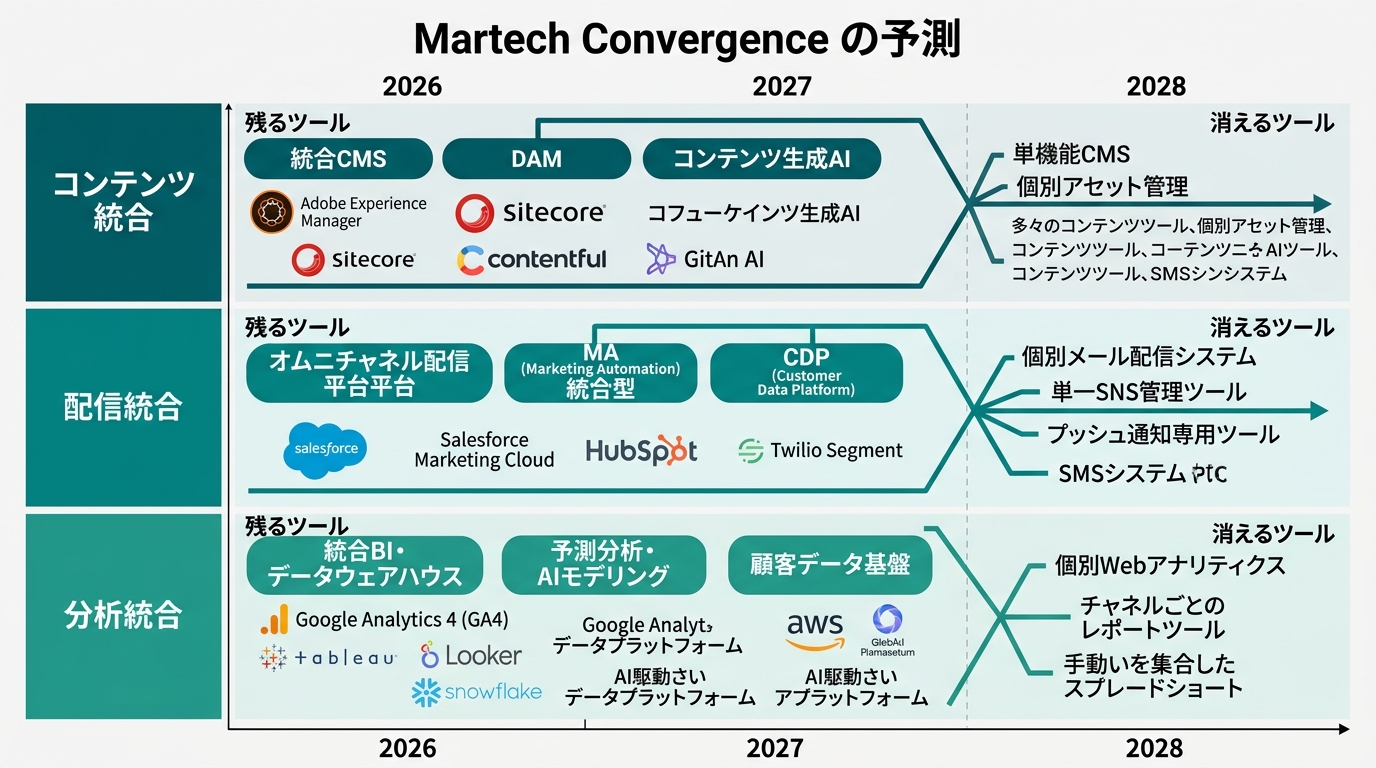

The Map in Six Months — Where Will Consolidation Strike Next

Let me venture a bit into prediction. Drawing on four months of market observation, I’ve assembled my own hypothesis for how martech consolidation will progress. These aren’t facts I can verify — read them strictly as my view.

[Confirmed facts] Adobe’s completion of the Semrush acquisition (April 28, 2026) and Ahrefs Social Media Manager’s official release (January 2026) are confirmed in primary sources. The following are hypotheses beyond that.

[Author’s hypothesis] Prediction 1: Email delivery tools will be fully absorbed into CRMs/MAs (within 2026)

Independent email delivery tools like Mailchimp, SendGrid, and ConvertKit. The motion of these being absorbed into HubSpot, Klaviyo, and Salesforce has already begun. The point when “signing a standalone email delivery contract” becomes rare may be close.

[Author’s hypothesis] Prediction 2: Video management tools will be consolidated into content platforms (2026–2027)

Video-specialized tools like YouTube analytics, TikTok operations, and reels management. There’s a chance integrated players like Ahrefs and Adobe move to absorb them. While video’s importance keeps rising, the need to separately contract a “video-only tool” may decline.

[Author’s hypothesis] Prediction 3: AI search analytics tools will merge into search platforms (2027 and beyond)

Independent AI search analytics tools like Profound and the GEO-related space. The direction of mounting integration pressure into existing search tools like Ahrefs and Semrush is visible. That said, this timeline has the highest uncertainty and is a domain that needs to be reassessed two years out.

If even one of the three predictions lands, the stack design you have today will need adjusting in six months. So when you sign tool contracts today, weight “annual flexibility” higher than “three-year contracts.” This is my rule of thumb, and the same pattern played out in the past CRM consolidation history.

Lastly, what matters in a consolidation phase is reading “what will remain” rather than “what will disappear.” Two kinds of tools remain. One is the core of an integrated platform. The other is the specialized tool that can coexist with an integrated platform. The “lukewarm multi-feature tool” stuck in the middle is in the most dangerous position.

Summary. Stack Decisions Run on Two Axes: “Market Movement” and “Your Own Work”

In yesterday’s article, I shared “decision criteria for subtracting from your own stack.” Today was the companion piece on “the consolidation phase of the market as a whole.”

Three points worth holding onto.

- Ahrefs Social Media Manager’s entry is not a solo event. It’s part of a market reshuffle happening in parallel with Adobe’s $1.9 billion Semrush acquisition, and martech is moving from “expansion” toward “consolidation” in 2026

- By analogy with CRM consolidation history, the consolidation phase completes in 3–5 years. Looking at the consolidation history of the 2010s, independent tools branched into one of three: “get acquired,” “niche down,” or “become all-in-one.” Tools stuck in the middle disappear

- Marketers have three options. Ride the wave, niche down with your own axis, or wait and see. Which to pick comes down to work style and need for data integration. Move with the premise that you’ll revisit the position you choose today in six months

This weekend, open the list of tools you’re using. Just decide, one by one, whether each gets “swallowed by the wave or survives.” If there’s a tool in a middle position, you create lead time to start looking for a replacement over the next six months to a year.

Less “what should I sign up for next” and more “by which axis do I keep what I already have.” This is martech stack design in a consolidation phase. In an era where the entire map will change in six months, hold onto your decision axis yourself. This has been the consistent argument from Nagi running through everything since the 4/24 marketing map article.

Sources

- Adobe Newsroom: Adobe to Acquire Semrush (announced November 13, 2025)

- Adobe Newsroom: Adobe Completes Semrush Acquisition (completed April 28, 2026)

- Ahrefs official: Social Media Manager

- PR TIMES: Ahrefs Social Media Manager officially released (January 22, 2026)

- Sprout Social official press release: Gen Z social search behavior survey (2025 Q2, 2,280 respondents in US/UK/Australia)

- Author’s observation: Martech market M&A and new feature release trends from January through May 2026

Related articles

- Ahrefs Social Media Manager: An Honest Report After Four Months of Use (previous day’s article)

- Ahrefs Started Doing Social Media Management. This Is the Signal for the Era When “SEO Leads Design Marketing as a Whole” (breaking)

- The 2026 Marketing Map Now Fits on a Single Page — A Strategy Document for the AI Search Era

- What People Managing SEO and Social Separately Are Quietly Losing in 2026

- What’s Happening in 2026 to Companies That Only “Took” AI Training

AIを使いこなせない方は、この先どんどん差がつきます。僕はAIエージェントを毎日動かして、壊して、直して、また動かしてます。そういう泥臭い実践の記録をここに書いてます。理論は他の方にお任せしました。僕は動くものを作ります。朝5時に起きてウォーキングしてからコードを書くのがルーティンです。