Cursor Hit $2B ARR in 3 Years. Then Fortune Called It 'Crossroads.' Here Are the Four Structural Reasons Why.

ARR $2B, $30B valuation, 67% of Fortune 500 as customers — yet Fortune titled their piece 'rapid rise and very uncertain future.' Breaking down Cursor's four structural vulnerabilities. Vibe-coding series #8.

What you'll learn in this article

- The key point to grasp before reading the full article

- How the issue changes the way developers should work next

- Which follow-up article is worth opening next

Let me just list the numbers.

ARR $2B. Reached in three years. Faster than Slack, Zoom, or Snowflake — the fastest B2B SaaS (enterprise cloud software) ramp in history. $30B valuation, $2.3B raised in Series D, 67% of Fortune 500 as customers, 150 million lines of code generated per day, $2B+ in fresh funding talks at a $50B valuation, and a $60B acquisition offer from SpaceX.

If you wrote that up, everyone would call it the most dominant growth company alive.

And yet, Fortune titled their March 2026 piece on the same company: “Cursor’s crossroads: The rapid rise, and very uncertain future, of a $30 billion AI startup.”

My first reaction was that an editor had slapped on a contrarian headline. $2B ARR and you say “uncertain future”? Come on.

But when I actually read the piece, Fortune’s reporter genuinely believed Cursor was at a crossroads. In my previous article (/en/blog/g2026051200015901/) where I compared five major vibe-coders, I labeled Cursor “the definitive IDE player.” That “IDE” label itself, I realized, was exactly the first crossroads Fortune was pointing to — and that was when I knew I had to dig deeper.

CEO Michael Truell is 25 years old. The view from inside that company looks nothing like the numbers from the outside. Today I’m unpacking that gap through four structural frameworks. Vibe-coding series #8: The Cursor corporate thesis.

The Numbers Are Record-Breaking. So Why Did They Write “Crossroads”?

First, let me lay out the metrics Fortune highlighted. Looking at these alone makes the “crossroads” framing even harder to understand.

| Metric | Value | Source |

|---|---|---|

| ARR (Jan 2025) | $100M | TechCrunch |

| ARR (Jun 2025) | $500M | TechCrunch (Anysphere $9.9B valuation) |

| ARR (Nov 2025) | $1B | Cursor official (Series D) |

| ARR (Feb 2026) | $2B | TechCrunch (multiple Anysphere sources) |

| ARR (end-2026 projected) | $6B+ | TechCrunch |

| Series D raised | $2.3B (Nov 13, 2025) | CNBC, Cursor official |

| Post-Series D valuation | $29.3B | CNBC |

| Additional round talks (Apr 2026) | $2B+ at $50B valuation | TechCrunch |

| SpaceX acquisition offer | $60B | Fortune (Apr 22, 2026) |

| Fortune 500 adoption rate | 67% | Fortune (Mar 21, 2026) |

| Daily lines of code generated | 150M (enterprise customers) | Fortune |

| Years since founding | 3 (Anysphere est. 2022) | Wikipedia |

Zero to $2B ARR in three years. To put that in perspective: Slack took 7 years to reach $1B in revenue. Zoom took 6. Snowflake took 8. Cursor blew past that threshold in under three years and kept climbing to $2B.

In SaaS circles, “Triple, Triple, Double, Double, Double” — tripling in the first two years, then doubling for three more — is the gold standard growth curve. Cursor rewrote it entirely.

That’s the “record-breaking” story. So what’s the “crossroads”? The four structural vulnerabilities that Fortune reporter Justin Waters surfaced in his interviews — that’s today’s main event.

Crossroads #1: Product Structure — Does an IDE-Centric Strategy Hold Up in the Agent Era?

What Fortune led with was a February 2026 episode on X (formerly Twitter): “Cursor is dead.”

It started when a startup called Valon posted that they’d stopped using Cursor. The fact that one company’s choice went viral was a sign that a vague, ambient anxiety about Cursor had been building. According to Fortune, that anxiety comes down to one thing: a suspicion that the future of coding isn’t the IDE (integrated development environment) — it’s autonomous agents.

I’ve touched on this before. In my article on economic structures and in my five-vibe-coders comparison, CLI-style tools like Claude Code, Codex CLI, and Devin are designed so developers don’t need to stay glued to an IDE (text editor). You give instructions, the AI works in the background, results come back. The relationship between engineers and their IDE has quietly shifted.

Cursor is a powerful IDE. That’s not in dispute. But the moment the assumption “developers use an IDE” breaks down, half of Cursor’s product value floats up in the air.

Truell obviously sees this risk. That’s why he shipped Composer 2 in May 2026 — Cursor’s own coding-specific model. A move toward being a model provider rather than just an IDE. I broke down the economics in detail here.

Even so, predictions are split. One VC spoke anonymously to Fortune: “The question isn’t whether Cursor will exist in 2027. It’s how much the IDE category itself will have shrunk by 2027.”

Crossroads #1 in a sentence: Does Cursor stay No. 1 in the IDE market and win there — or does the IDE market itself shrink until winning it no longer matters?

Crossroads #2: Revenue Structure — $2B ARR, But Thin Gross Margins

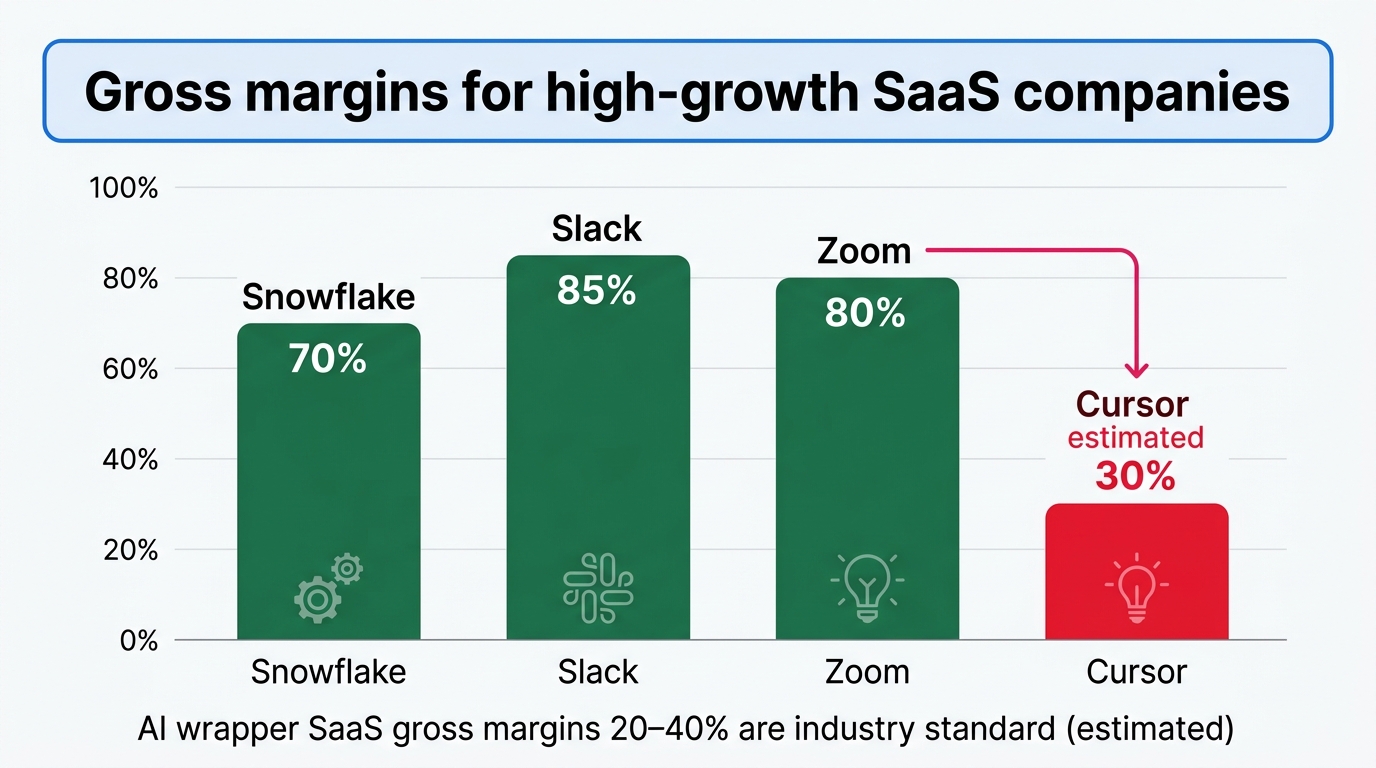

Headline ARR numbers are flashy. What actually matters is how much gross profit remains after the revenue line.

Fortune, and TheNextWeb reporting alongside it, wrote that Cursor’s payments to OpenAI and Anthropic for model usage “take the majority of revenue.” No specific figure was disclosed. But applying SaaS industry benchmarks: AI wrapper services (no proprietary model) typically run at 20–40% gross margins.

If Cursor’s gross margin is 30%, then on $2B ARR the actual take-home is roughly $600M. To generate a return for the investors who put in $2.3B at Series D, the valuation needs to keep climbing or there needs to be a liquidity event via IPO.

This is where Composer 2 makes economic sense. With a proprietary model, gross margins could climb to 50–70%. The reason Truell launched Composer 2 as “early access” at one-tenth the price has an economic inevitability behind it: fix the margin problem. I detailed that logic here.

But building proprietary models carries its own risks. Anthropic and OpenAI pour billions annually into model research. If Cursor wants to compete on the same field, the $2.3B from Series D goes to R&D. And at that point, can they beat Anthropic’s Claude? Right now, the honest answer is no.

Crossroads #2: Does Cursor become a model provider and fix the margin problem — or stay as an AI wrapper, betting that ARR growth can outrun thin margins?

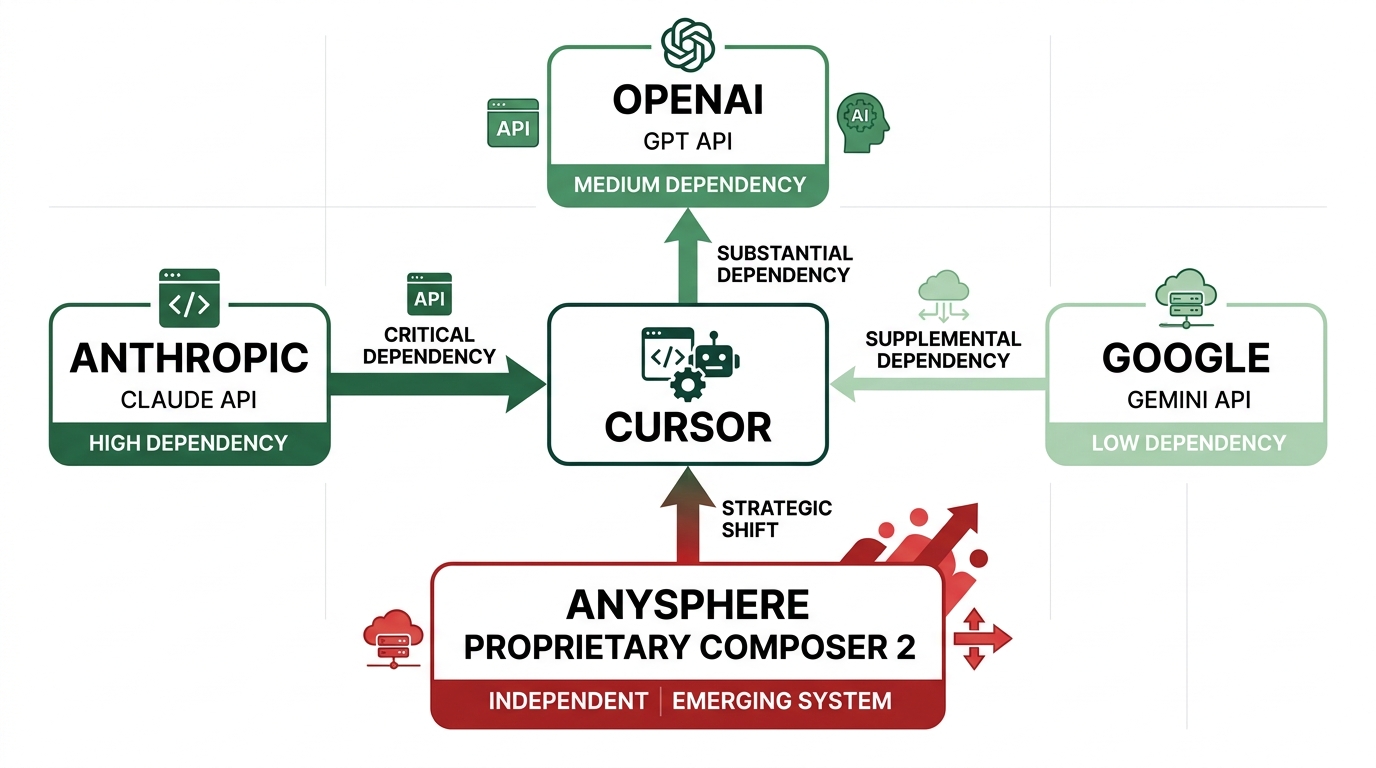

Crossroads #3: Dependency Structure — The Day Anthropic Raises Prices, Cursor Is in Trouble

This one hit me the hardest.

Cursor’s default model has long been Anthropic’s Claude series. GPT-4.5 and Gemini 2.5 became selectable in late 2025, but user surveys show Claude Opus/Sonnet still dominate overwhelmingly.

Fortune quoted a veteran from the industry: “If Anthropic doubled the Claude API unit price tomorrow, Cursor faces a forced decision: pass the cost to users and lose them, eat it and cut margins in half, or force-migrate everyone to Composer 2.”

When I read that, something clicked — the kind of recognition you get from years in CS work. I’ve watched it happen to companies on top of Salesforce, HubSpot, Slack. Platform owners change pricing or policy, and overnight the businesses built on top are cornered.

From Anthropic’s perspective, Cursor is one of their largest API customers. It’s conceivable that more than half of Cursor’s ARR flows right back to Anthropic in API fees (estimated). Cursor is a cash cow for Anthropic — and simultaneously a competitor to Claude.ai. If Anthropic beefs up Claude.ai’s developer features in H2 2026, they’re in direct competition with Cursor.

And here’s what’s worth remembering: Anthropic has already shipped Claude Code. That’s effectively Anthropic releasing a Cursor substitute themselves. If Anthropic seriously starts funneling users toward Claude Code, Cursor ends up competing with Anthropic on Anthropic’s own turf.

Crossroads #3: Can Cursor break free from dependency? Will Composer 2 get there in time? Or does Cursor keep running — Anthropic-dependent, with Anthropic holding the pricing lever?

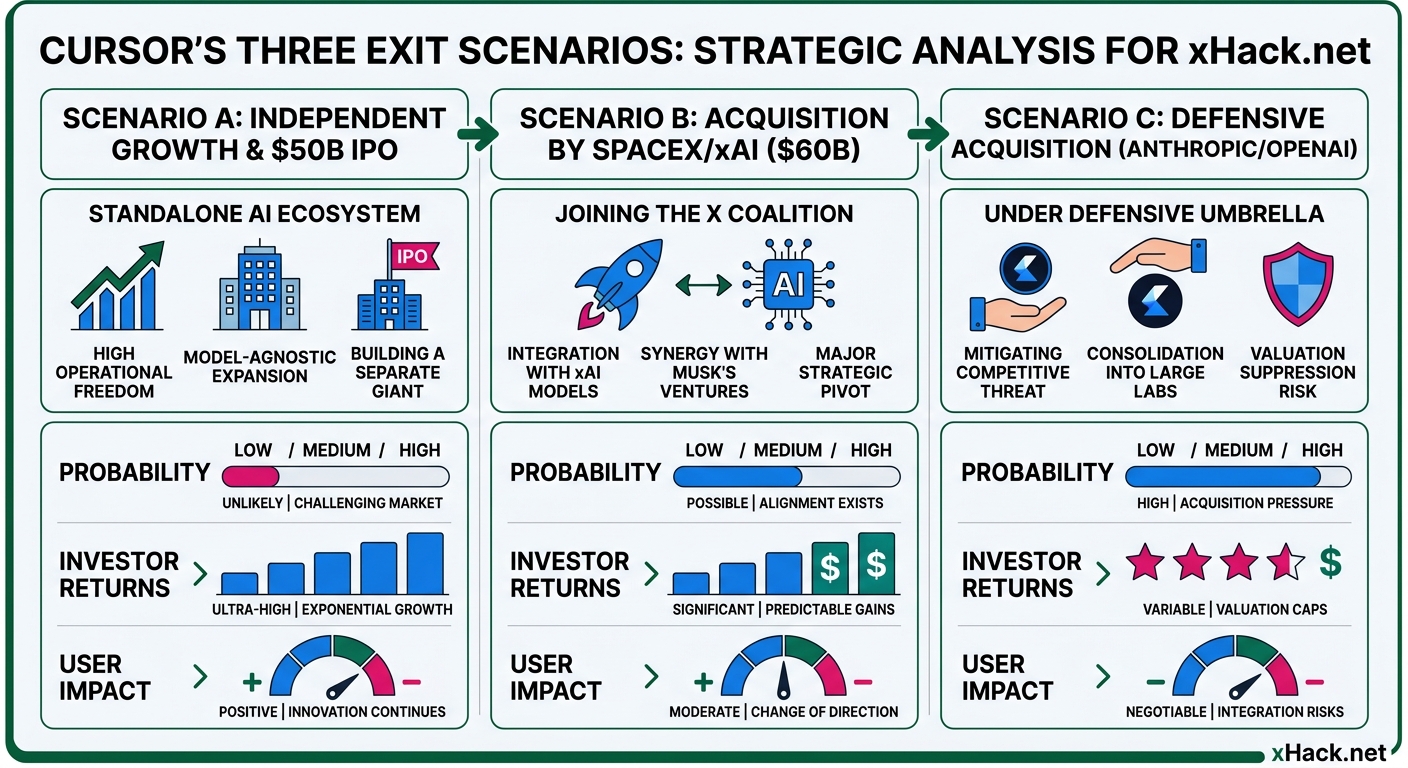

Crossroads #4: Exit Structure — $60B SpaceX Acquisition or $50B IPO?

In April 2026, Fortune reported that SpaceX had floated a $60B acquisition of Cursor. TechCrunch, in the same month, reported Cursor was in talks for $2B+ at a $50B valuation.

These two aren’t contradictory. The acquisition offer likely created a negotiating card to push the independent valuation up — a way to say “we’re worth $60B to SpaceX, so give us $50B to stay independent.”

What’s interesting is why SpaceX would want Cursor at all. SpaceX is an aerospace company. The direct business synergy with a coding tool is thin. But for Elon Musk’s xAI, Cursor is immensely attractive. Grok model + Cursor = a vertically integrated coding platform to rival the Anthropic/OpenAI coalition.

The real substance of the SpaceX acquisition offer is a coalition-choice decision. Stay in the Anthropic/OpenAI camp — or move to the xAI/Tesla/SpaceX camp. The $60B price tag isn’t just a number; it includes a “defection bonus.”

Truell is 25. His founder equity percentage hasn’t been disclosed, but post-Series D he likely holds 10–20%. A $60B acquisition means $6–12B personally. A $50B IPO doesn’t give him immediate liquidity but lets him keep building Cursor on his own terms.

If I were 25 and someone put $6B in front of me, I’d be tempted too. And yet Truell has not publicly said he’s selling Cursor.

Crossroads #4: Accept $60B and join a camp — or maintain independence at $50B and target an IPO? The decision deadline is probably end of 2026.

Three Things Vibe-Coders Should Decide Now

That was the Cursor-side story. Let me finish with what we on the using side — vibe-coders — should be thinking about.

I use Cursor every day. Which means this “crossroads” is personal. If Cursor gets acquired, pricing models and model options could all change. Three things to settle now.

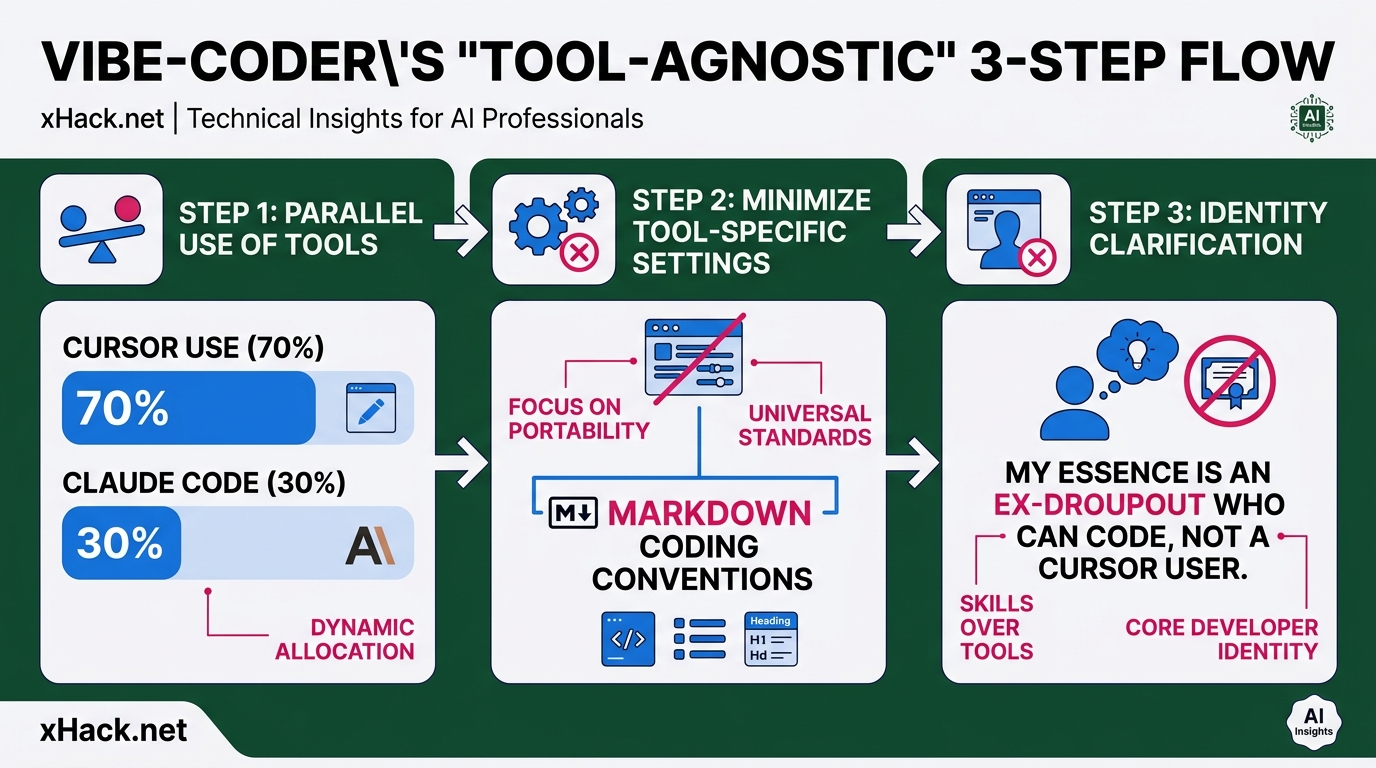

#1: Build a development workflow that doesn’t depend only on Cursor

So you’re not stuck if something happens to Cursor: touch CLI tools (Claude Code, Codex CLI) at least once a week. Not necessarily on real projects — just keep the muscle memory for how to issue instructions and run things from a terminal. My own split is intentionally 70% Cursor, 30% Claude Code.

#2: Keep your code assets “tool-agnostic”

Over-reliance on Cursor’s extensions and rules (.cursorrules) raises migration cost when you need to switch. I keep my project’s coding conventions in plain Markdown, without depending on Cursor-specific features. That alone shrinks a two-day migration to two hours.

#3: Question the feeling that “the tool has a soul”

When I first started using Cursor, it genuinely felt like a genius engineer had taken up residence in my editor. That feeling was real. But looking back, it wasn’t that “Cursor was exceptional” — it was that “the combination of 2025-era AI models + IDE was exceptional.” By 2027, some other combination will likely occupy that position.

Fall too hard for a tool, and when the tool changes, you have to change yourself. My core identity is “an ex-dropout who can code,” not “a Cursor user.” I remind myself of that distinction every week.

Conclusion — “Crossroads” Is Not a Warning of Failure

The “crossroads” Fortune wrote about isn’t a prediction that Cursor will fail. It’s a clear-eyed accounting of the fact that even after this much growth, four major forks lie ahead.

- Product structure crossroads: IDE-centric vs. agent-centric

- Revenue structure crossroads: proprietary model vs. AI wrapper

- Dependency structure crossroads: Anthropic-dependent vs. independent

- Exit structure crossroads: SpaceX acquisition vs. IPO independence

As vibe-coders, we’ll learn how each crossroads resolves through Cursor’s update notes. If pricing changes, that’s the signal that crossroads #2 has been decided. If model options narrow, that’s crossroads #3 resolving.

What CS work taught me is that the people who model platform-owner strategy shifts and prepare hedges in advance are the ones who win long-term. Rather than going all-in on Cursor, the ex-dropout-turned-engineer’s survival strategy is this: observe Cursor’s crossroads as they unfold, and layer your development workflow accordingly.

Three years, $2B ARR, the fastest B2B SaaS in history — and still “a very uncertain future.” That dissonance is worth sitting with. I plan to keep using Cursor a while longer, with eyes open.

Sources

- Fortune: Cursor’s crossroads (Mar 21, 2026)

- Fortune: SpaceX–Cursor $60B deal (Apr 22, 2026)

- Fortune: Cursor’s 25-year-old CEO (Apr 22, 2026)

- TechCrunch: Cursor $50B valuation talks (Apr 17, 2026)

- CNBC: Cursor Series D $29.3B (Nov 13, 2025)

- TechCrunch: Anysphere $9.9B Series C (Jun 5, 2025)

- TheNextWeb: Cursor $2B ARR in 3 years

- Wikipedia: Anysphere

Related Articles

- /en/blog/g2026051200015901/ — Vibe-coding series #7: Five major vibe-coders compared

- /en/blog/g2026051100015601/ — Vibe-coding series #6: Cursor Composer 2 economics breakdown

- /en/blog/g2026051000015301/ — Vibe-coding series #5: Cursor CEO’s “house of cards” warning

- /en/blog/g2026050900015001/ — CodeGuard trilogy finale

- /en/blog/g2026050400013501/ — Structural theory for the vibe-coding era

正直、一度エンジニアは諦めました。新卒で入った開発会社でバケモノみたいに優秀な人たちに囲まれて、「あ、私はこっち側じゃないな」って悟ったんです。その後はカスタマーサクセスに転向して10年。でもCursorとClaude Codeに出会って、全部変わりました。完璧なコードじゃなくていい。自分の仕事を自分で楽にするコードが書ければ、それでいいんですよ。週末はサウナで整いながら次に作るツールのこと考えてます。